Merchant Onboarding in 2026: RBI Compliance, UPI Scale & Risk-Intelligent Frameworks for India

Date Published

Table of Contents

- What is Merchant Onboarding?

- Importance of Merchant Onboarding

- Core Components & Key Players of Merchant Onboarding

- Step-by-Step Guide on the Merchant Onboarding Process

- Technology & Automation Trends Shaping Onboarding in 2026

- Compliance, Risk & Security Considerations

- Challenges in Merchant Onboarding in 2026

- Paradigm Shift in Merchant Onboarding in 2026

- What Should a 2026-Ready Merchant Onboarding Framework Look Like?

- Key Takeaway

- FAQs

With the increase in technological advancement and the aggressive growth of the digital-first economy, businesses have a lot of dependency on seamless payment methods in order to give a seamless experience to their customers. At the core of this capability remains the process of merchant onboarding.

It is definitely a foundational step enabling businesses to connect with Payment Aggregators (PAs) and begin processing payments for their customers. This process goes beyond the paperwork and serves as a bridge between the financial ecosystem and the merchant. If the merchant onboarding system is well-structured, it ensures that only legitimate businesses become a part of the critical payment network, thereby reducing the risks of fraud, financial crime, and non-compliance with regulations.

As there is a significant increase in the global shift towards cashless transactions, the PAs must strike a balance. The journey of merchant onboarding not only needs to be user-friendly and fast but also comprehensive enough to protect the network. If the merchant onboarding process is implemented correctly, it not only helps build trust and support regulatory compliance but also accelerates the ability of the merchant to accept payments and contribute to the growing economy of the country. In this blog, we will do an in-depth analysis of what merchant onboarding is, why it is important, the key components of the process, and what are the major challenges this space is facing.

What is Merchant Onboarding?

Merchant Onboarding Process: How PSPs Verify Businesses for Secure and Compliant Digital Payments

The set of activities conducted by the PAs to assess, verify, and show green flags to new merchants before they can accept new payments is referred to as the merchant onboarding process. This is done in order to confirm that the merchant is a legitimate business that can handle payments and meet all the regulatory and compliance standards. At the very core of merchant onboarding lies identity verification (such as Know Your Business or KYB and Know Your Customer or KYC checks) with risk assessment and ongoing monitoring efforts to ensure safety across the entire payment network. Merchant onboarding paves the way for a long-term relationship between the merchant and the aggregator. It also plays a crucial role in protecting the payment ecosystem by filtering out high-risk entities and thereby helping to reduce financial crime, fraud, and reputational harm for all parties involved. Although the specific steps can vary across industry and geography, the overarching goal remains the same, i.e., to allow trustworthy businesses to engage in electronic payments quickly and securely.

Merchant onboarding is the first and most critical step in the merchant acquiring business, as it determines who can legally and securely process digital transactions. There is another term that is talked about whenever merchant onboarding is discussed. It is called merchant acquiring.

What is Merchant Acquiring?

Merchant acquiring refers to the process through which acquiring banks and payment aggregators enable merchants to accept card, UPI, and digital payments. While the merchant onboarding implies verifying and approving the merchant, merchant acquiring is about enabling the merchant to process payments successfully. Now, let’s understand why we need merchant onboarding and its importance.

Importance of Merchant Onboarding

In 2026, the importance of merchant onboarding and the broader merchant ecosystem has never been clearer. In India, the Unified Payments Interface (UPI) has accelerated the need for creating the world’s largest merchant network, with over 678 million UPI QR codes deployed and millions of small kiranas and service providers transitioning to digital acceptance models. This extraordinary growth stands witness to how a smooth and streamlined merchant onboarding process can drastically lead to business expansion across the country, enabling merchants across all economic strata to participate in the digital economy without any requirement for traditional infrastructure or high costs.

Merchant onboarding also matters because it is instrumental in building confidence and trust across the entire payment ecosystem. In today’s regulatory climate, authorities like the Reserve Bank of India (RBI) are tightening security by mandating robust authentication standards, such as multi-factor authentication for digital transactions, to reduce the risk of fraud and unauthorized access. These requirements will come into effect from April 2026, reinforcing the requirement for onboarding workflows that verify merchant identity and secure consumer interactions, thereby helping to protect both businesses and their customers.

The gaps in onboarding often lead to transaction failures flagged as invalid merchant or invalid merchant details. A thoughtful merchant onboarding process is one that balances ease of entry with strong compliance and security. It is now a need of the hour for both the payment providers and regulators.

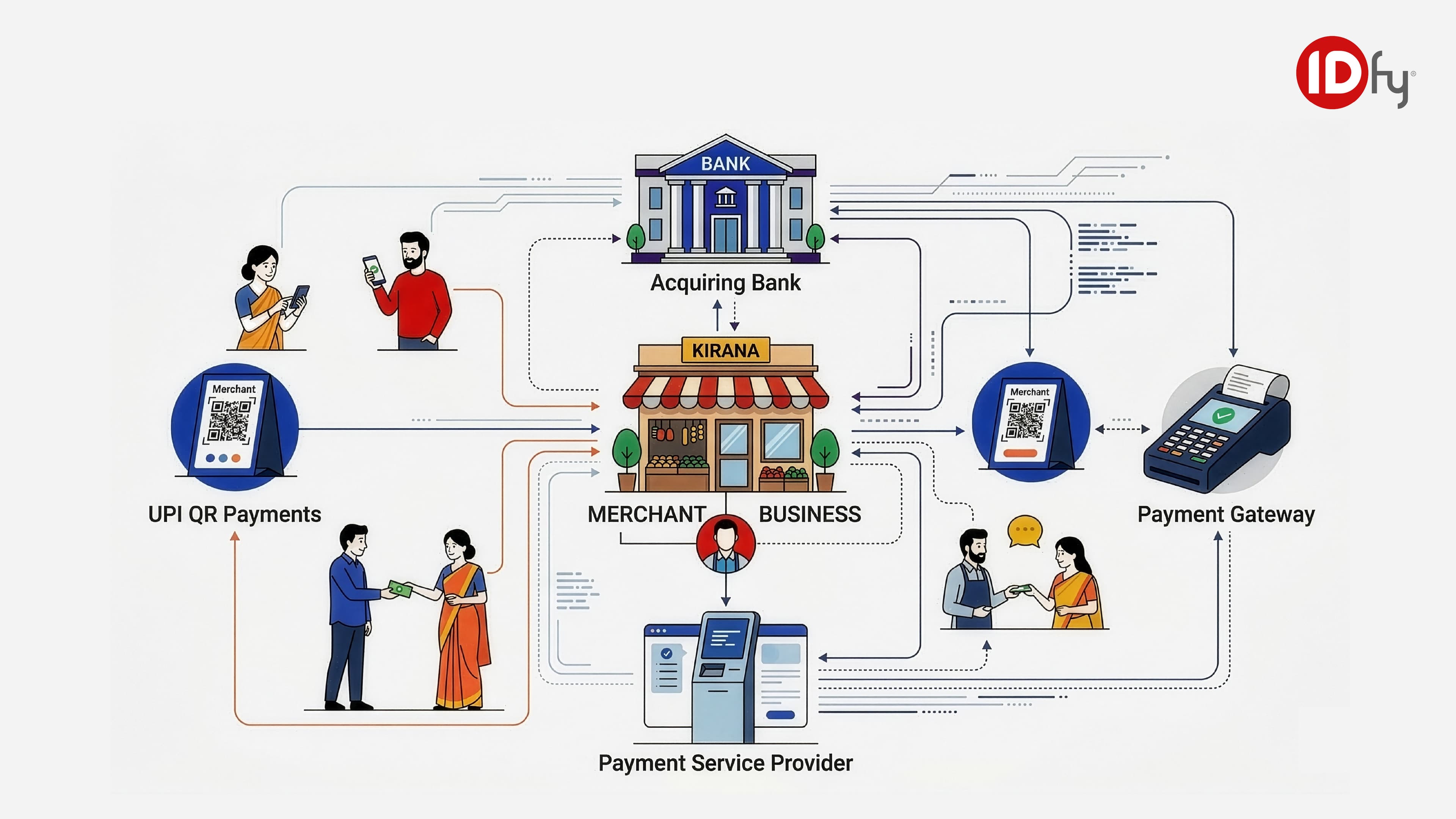

Core Components & Key Players of Merchant Onboarding

The key components of the merchant onboarding process are:

- Merchants: Merchants are businesses or service providers that want to accept digital payments from customers. The process is initiated by them by submitting business details, ownership information, and financial data.

- Payment Aggregators (PAs): PAs facilitate payment processing for merchants. They manage onboarding workflows, conduct identity verification, assess risk, and ensure regulatory compliance. PAs also handle transaction authorization, clearing, and settlement, making them central to the merchant onboarding lifecycle.

- Acquiring Banks: Acquiring banks are the ones that underwrite merchant accounts and assume financial risk during transactions. They are also responsible for assessing the merchant’s business model, risk exposure, and compliance before approving the payment processing capabilities.

- Payment Gateways: The technical infrastructure for secure transaction data between the merchants and the financial institutions is provided by the payment gateways. Sensitive information is encrypted by these gateways, enabling smooth integration during account setup.

- Card Networks & Issuing Banks: Card networks are responsible for establishing transaction standards, while issuing banks are responsible for authorizing customer payments.

- Core Process Components: Alongside these key players, the merchant onboarding process also includes business information collection such as KYC and KYB verification, risk underwriting, compliance screening, technical integration, and ongoing monitoring. Together, these elements ensure that merchants can accept payments securely while protecting the integrity of the broader financial ecosystem.

Step-by-Step Guide on the Merchant Onboarding Process

Step-by-Step Merchant Onboarding Process: The 7 Stages From Data Capture and Identity Verification to Payment System Integration and Account Activation.

The merchant onboarding process is a structured journey that enables a business to begin accepting digital payments in a secure and compliant manner. Here is a step-by-step guide to the entire merchant onboarding process:

- Gathering Business Information: The objective of this step is to collect accurate and complete details about the merchant and its owners. Details such as business registration number, tax identification numbers (such as PAN and GST), bank account information, and ownership documentation are required. For individual proprietors, identity documents such as Aadhaar or other government-issued IDs are required. Modern-day merchant onboarding platforms streamline this stage through digital forms, API integrations, and real-time database verification. Automated checks also come in handy to validate the tax numbers, confirm registration status, and reduce manual errors, thereby ensuring that the onboarding process starts with verified and structured information.

- Application Submission: The primary objective of this step is to formally initiate the relationship between the merchant and the payment provider. The merchant is required to submit a formal application requesting payment processing services. This step includes agreeing to pricing terms, settling timelines, transaction fees, and platform policies. Digital merchant onboarding systems often provide guided workflows that ensure all mandatory fields and documents are submitted correctly.

- Identity Verification (KYC and KYB): The main intent of this step is to authenticate the legitimacy of the business and its owners. Identity verification serves as a critical component of the entire merchant onboarding process. Payment providers validate the credentials of the business via Know Your Business (KYB) and Know Your Customer (KYC). This also involves document authentication, database cross-checks, biometric verification, and liveness detection. Advanced systems also leverage AI-powered tools to detect forged documents and flag inconsistencies. This step ensures that fraud is prevented, there’s no identity theft, and there’s no unauthorized access to payment systems.

- Credit and Risk Assessment: The primary goal of this step is to evaluate the merchant’s financial stability and his exposure to risk. PAs assess the creditworthiness of the merchants, their transaction history, industry risk category, and whether there are any prior chargeback records. Automated underwriting tools analyze financial statements, credit scores, and behavioral risk signals to create a complete risk profile. Based on this assessment, the PAs decide the transaction limits, rolling reserves, or whether there are any additional requirements for monitoring.

- Compliance and Regulatory Screening: Merchants are screened against anti-money laundering (AML) lists, sanctions databases, and regulatory requirements. In India, this may also involve checks that are aligned with RBI guidelines and other applicable regulations. The merchant onboarding system helps in verifying whether the business model is compliant with industry-specific rules, along with consumer protection laws. This step safeguards both the payment provider and the merchant from both legal and reputational risks.

- Payment System Integration: This is the step where the merchant’s systems are integrated with the payment gateway or payment aggregator. This includes configuring point-of-sale systems, e-commerce platforms, or mobile applications. Proper technical setup is done, which ensures seamless authorization, processing, and settlement of payments.

- Final Agreement and Account Activation: This step marks the end of the merchant onboarding process and enables transactions. The final stage involves signing service agreements and confirming operational readiness. Once documentation is completed and systems are configured, the merchant’s account is activated. The business can then begin accepting payments immediately. Ongoing monitoring continues even after activation to ensure compliance and manage evolving risks.

Technology & Automation Trends Shaping Merchant Onboarding in 2026

The merchant onboarding process is reshaping with the advancement in technology and automation, which is playing a huge role in eliminating friction, reducing turnaround time, and improving compliance. The adoption of smart automation tools is one of the biggest shifts that we are seeing in merchant onboarding in 2026. Manual checks are being replaced by automated document validation and identity verification, thereby reducing the time required to approve applications of all sizes from days to minutes. This shift has paved the path for a significant shift in the onboarding timelines, making the entire onboarding journey for businesses faster and more predictable.

Artificial intelligence (AI) and machine learning are playing a significant role in driving this transformation. Starting from risk scoring, real-time fraud detection, to anomaly identification, everything is now AI-powered without the need for human intervention. By integrating multi-modal biometric authentication, such as facial recognition and device signals, platforms are reducing fraud while keeping onboarding smooth and secure.

Compliance, Risk & Security Considerations

Since always, compliance has been a defining pillar for the entire merchant onboarding process. Under the RBI’s updated Master Directions for Payment Aggregators, onboarding can no longer rely on light-touch digital KYC alone. Payment aggregators must conduct stronger due diligence, including mandatory Contact Point Verification (CPV), enhanced background checks, and demonstrable “fit and proper” assessments of merchants and their key stakeholders.

This shift is a reflection of a broader regulatory priority, which is merchant risk, especially in offline and hybrid models. Aggregators are now required to validate the actual line of business, authenticity of the ownership, and operational presence before activation. Compliance has moved away from just avoiding penalties and is now playing as a growth driver. Weak onboarding controls can lead to forced merchant offboarding, frozen settlements, reputational damage, and direct Gross Transaction Value (GTV) erosion. In a high-volume ecosystem, scalable compliance infrastructure is now a growth enabler, not a bottleneck.

Another most often ignored but critical risk is Merchant Category Code (MCC) misclassification. An MCC helps in determining how a merchant is categorized, their MDR, cashback eligibility, the tax treatment they receive, and if there’s any compliance scrutiny. A wrong classification can result in incorrect fee structures, loss of customer rewards, and grave consequences such as regulatory complications.

For instance, mislabeling a travel transaction as rent can alter rewards, tax implications, and risk assessment. Regulators are now expecting tighter MCC validation during merchant onboarding through CPV, business verification, and AI-based checks. MCC accuracy is no longer a backend detail; it now directly impacts revenue integrity, compliance posture, and customer trust.

Challenges in Merchant Onboarding in 2026

The merchant onboarding process continues to be one of the most complex aspects of the digital payments ecosystem. Here are some key challenges that this space is facing:

- Coordinating a smooth onboarding flow along with fraud prevention: One of the major challenges is to strike the right balance between a smooth onboarding experience and effective fraud prevention. While a streamlined process attracts more merchants and accelerates revenue growth, a lack of sufficient risk checks can expose the PAs to financial crime and regulatory penalties. Efficient onboarding needs to have robust identity verification, background checks, and risk signals analysis, which often compete with the merchants’ expectations for speed.

- Keeping up with regulatory changes: Another major challenge for merchants onboarding is keeping up with the changing regulatory frameworks. Ensuring documentation accuracy and managing sanctions checks can be very resource-intensive as well as time-consuming. Manual processes not only create bottlenecks but also increase operational costs and heighten the risk of human error. Automated solutions that leverage machine-assisted verification, real-time data cross-checks, and risk scoring help solve these pain points to a great extent.

- Technical complexity: Integration and technical complexity still remain significant hurdles, especially for mid-sized merchants who have no dedicated IT teams. Flexible integration tools, well-documented APIs, and guided technical support can drastically reduce this friction and also help in shortening time-to-value.

Paradigm Shift in Merchant Onboarding in 2026

The perspective towards merchant onboarding saw a drastic change in 2025. Now, onboarding no longer remains a one-time event but has gradually evolved into a continuous relationship that extends well beyond account activation. Traditionally, merchant onboarding would come to an end once the merchant was authorised to process payments; however, with the new guidelines in place, an increase in complex risk profiles, and increased demand for customer satisfaction, post-onboarding is an equally critical phase as the onboarding itself.

Post-onboarding activities such as ongoing identity verification, dynamic risk assessment, behavioural monitoring, and real-time feedback loops have also become a part of onboarding. As merchants begin to process payments, their behaviour may also reveal unforeseen risk and compliance issues. Their activity patterns should be continuously evaluated along with updating risk scores.

Merchants today also expect proactive communication and transparency about the status of their application and compliance checkpoints. Providers that deliver these structured updates and provide robust post-onboarding support are able to build stronger relationships with them. This ongoing engagement, from automated nudges to intelligent workflows that adapt merchant journeys based on risk and behaviour, turns onboarding into a living process rather than just a point-in-time milestone. In 2026, post-onboarding is essentially the new onboarding.

How Should a 2026-Ready Merchant Onboarding Framework Look Like?

Merchant onboarding can no longer be a linear or documentation-heavy process. Instead, it must be a risk-intelligent, omnichannel, and continuously monitored process. Here’s how the framework of the new-age merchant onboarding solution looks:

- Multi-Channel Acceptance: With QR, SoftPOS, and auto-pay becoming the default rails in India, onboarding should also be able to support instant digital activation across online and offline channels. Merchants should be able to onboard across multiple channels and through various journeys, such as DIY, video-assisted, or RM-led journeys, without any friction. India is becoming UPI-first, and so should the onboarding journey be.

- Strong Regulatory Baseline: Compliance must be adhered to from Day 0. This includes starting from KYC/KYB, UBO identification, to PAN–CIN–GST validation, CPV, court, and eFIR checks, AML screening, and dynamic risk categorization.

- Accurate Line-of-Business & MCC Validation: Given the systemic risks of MCC misclassification, frameworks should be able to validate declared business activity with the help of AI-based website scans, shopfront image analysis, and inventory profiling to ensure correct categorization.

- Risk-Based Monitoring: Onboarding should not be done just at the beginning, but should gradually evolve into a seamless transition of ongoing monitoring.

- Revenue Intelligence Layer: Modern frameworks should also be able to unlock growth by identifying hidden affluence, enabling cross-sell, better settlement terms, and lending readiness.

This is where IDfy’s Merchant Onboarding solution comes in handy. By combining omni-channel onboarding, AI-driven MCC detection, digitized CPV, enhanced due diligence, and continuous risk monitoring, IDfy is now enabling financial institutions to onboard merchants up to 85% faster while strengthening fraud controls and compliance.

Key Takeaway

Merchant onboarding in 2026 is no longer about activating accounts quickly; it is the foundation of sustainable merchant acquiring. A modern merchant acquiring business must:

- Embed strong merchant KYC.

- Prevent invalid merchant risks.

- Monitor merchant fraud proactively.

- Enforce correct MCC mapping.

- Apply intelligent merchant transaction limits.

- Automate compliance screening.

Merchant onboarding is no longer just about activating accounts quickly; it’s more about building a scalable and risk-intelligent foundation for growth. With UPI-led expansion, RBI’s tighter Payment Aggregator norms, mandatory CPV, enhanced due diligence, and stronger authentication requirements, the merchant onboarding process must be balanced with speed, compliance, and fraud prevention in parallel.

Weak KYC, poor risk categorization, or MCC misclassification are no longer minor operational errors. They directly impact interchange, MDR, tax treatment, customer rewards, regulatory exposure, and ultimately the GTV. At the same time, onboarding cannot become so heavy that it slows down merchant acquisition or increases drop-offs.

The winning framework in 2026 is omni-channel, AI-enabled, and risk-based merchant onboarding. It does not just mitigate risk, but it also unlocks revenue through smarter merchant profiling and lifecycle intelligence.

If you are also rethinking your merchant onboarding strategy, reach out to us at shivani@idfy.com.

Frequently Asked Questions (FAQs)

- What is merchant onboarding?

The set of activities conducted by the payment aggregators (PAs) to assess, verify, and show green flags to new merchants before they can accept new payments is referred to as the merchant onboarding process. - Why is merchant onboarding important?

Effective merchant onboarding helps establish trust, enhances security, and reduces fraud risk by verifying business identity and compliance. It also ensures that merchants can operate within regulatory frameworks while providing a seamless payment experience for their customers. - What documents are typically required for merchant onboarding?

The most commonly required documents for merchant onboarding include business registration certificates, PAN card of the business or owner, bank account details, identity proof (like Aadhaar or passport), address proof, GST certificate, and information about the merchant’s website or app. - How long does the merchant onboarding process usually take?

The duration can vary depending on the provider and the completeness of documents. It can range from a few hours to several days, based on several factors such as verification complexity, regulatory checks, and technology used. - What role does KYC play in onboarding?

KYC verifies the merchant’s identity by validating key documents and ownership. It is a foundational step to prevent fraud and unauthorized access while building confidence in the payment ecosystem. - Can merchant onboarding services be automated?

Yes. Automation technologies like AI, machine learning, and OCR significantly speed up document verification, compliance checks, and risk assessments, improving accuracy and reducing manual workload.

Digital merchant onboarding leverages technology to simplify and speed up the process. By using digital tools such as online application

Customer onboarding has become a key idea in the quickly changing business and technological world. Today, we find ourselves in the midst of a digital revolution that is transforming the way businesses welcome and integrate new consumers.