Buy Now Pay Later (BNPL) in India: How It Works, Risks, and Future Trends

Date Published

India's digital payments story is one of the most consequential financial transformations of the past decade. UPI crossed 18 billion monthly transactions in 2024. Mobile-first commerce is no longer a trend; it is the default. And at the intersection of this infrastructure boom and a massive underserved credit market, Buy Now Pay Later has found its most fertile ground.

BNPL is not simply a consumer convenience feature. For fintechs and merchants, it is a strategic lever that reshapes checkout economics, customer acquisition cost, and average order value in a single integration. For compliance and risk teams, it is a product category that demands rigorous underwriting, fraud controls, and regulatory alignment. For payment operations leaders, it is a new layer of complexity sitting between the payment gateway, the lending partner, and the consumer's repayment cycle.

This guide offers a definitive, operationally grounded analysis of BNPL in India: how it works, what the business models look like, where the risks concentrate, and where the ecosystem is heading over the next three to five years.

What Is Buy Now Pay Later?

Buy Now Pay Later is a short-term consumer financing product that allows a customer to complete a purchase immediately and repay the cost over a defined period, either in a lump sum after a grace period or in structured installments. The defining characteristic is the deferred payment obligation created at the point of transaction, rather than at the point of application.

That distinction matters. Traditional lending involves an application, a disbursement, and a subsequent purchase. BNPL inverts this sequence: the purchase event itself triggers the credit. The underwriting happens in real time, invisibly, at checkout.

In India, BNPL sits within the broader digital lending ecosystem. Providers span several categories: pure-play fintechs such as LazyPay, Simpl, and ZestMoney; NBFC-backed platforms like KreditBee and EarlySalary; ecommerce giants with proprietary deferred payment products such as Amazon Pay Later and Flipkart Pay Later; and wallet-linked postpaid products like Paytm Postpaid. Banks including HDFC, ICICI, and Axis have entered the space through installment conversion features tied to existing credit card infrastructure. The RBI's Digital Lending Guidelines have increasingly formalized this landscape, requiring that any deferred payment product backed by a credit line must be structured and disclosed as a loan from a regulated entity.

The popular mental model of BNPL as "free credit at checkout" is accurate for the consumer experience but misleading about the underlying economics. Zero-cost EMI structures are subsidized by the merchant. Interest-bearing plans generate direct revenue for the lender. The consumer financing appears seamless precisely because the commercial arrangements between the BNPL provider, the lending partner, and the merchant are pre-negotiated and invisible to the buyer.

Post-UPI, BNPL adoption accelerated because the infrastructure for instant digital identity verification, payment rails, and merchant integration already existed. BNPL providers did not need to build a new payment network; they layered a credit decision engine on top of one that was already ubiquitous.

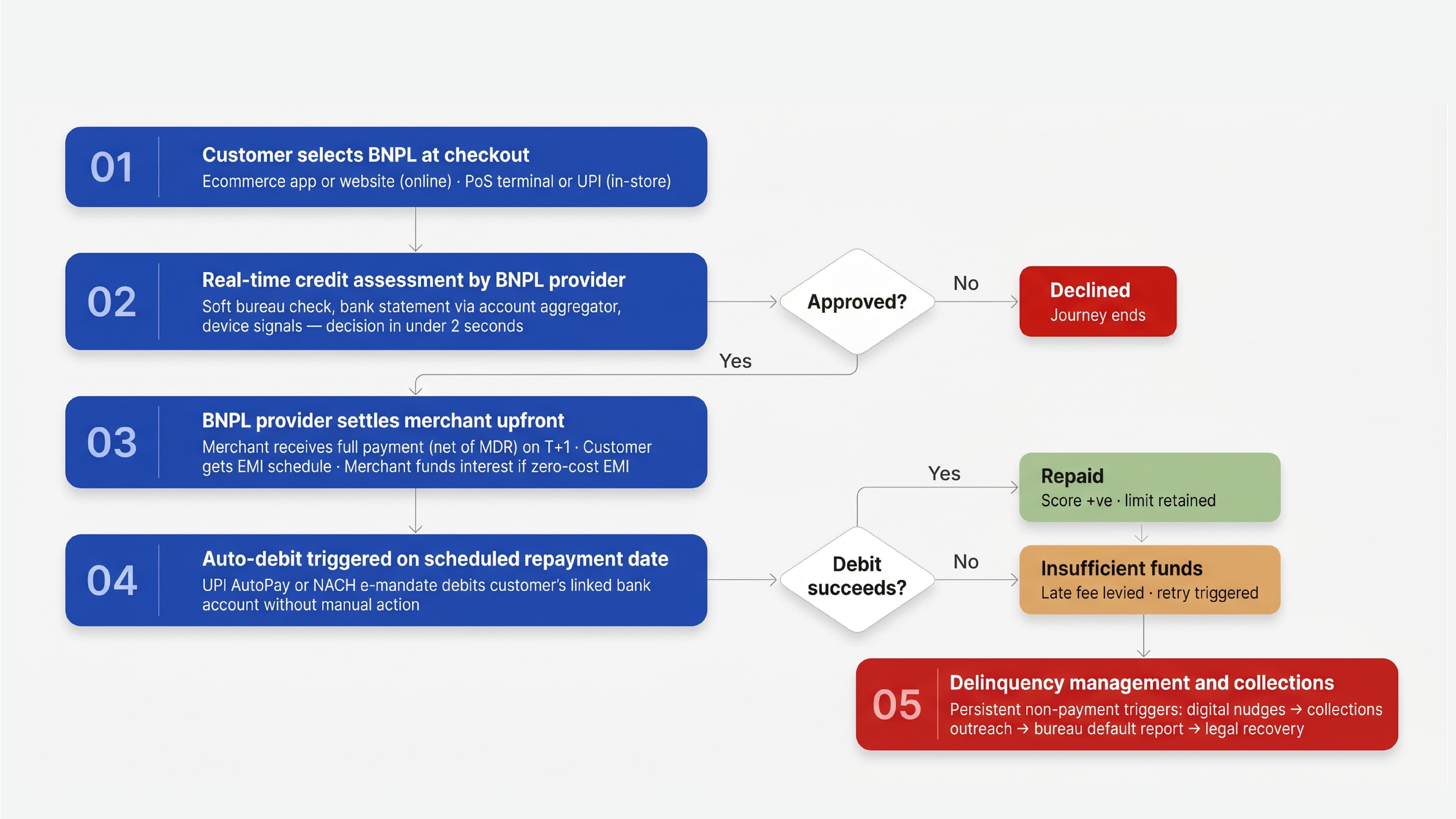

How BNPL Works in India — The Operational Flow

Understanding BNPL operationally requires tracing the transaction across five distinct stages. Each stage has its own infrastructure, risk exposure, and commercial implication.

Buy Now Pay Later (BNPL) Workflow in India: From Checkout Approval to EMI Repayment and Collections

- Step 1: Customer Selects BNPL at Checkout

The customer encounter with BNPL begins at the checkout screen, whether on an ecommerce platform, a merchant app, or increasingly at a physical point-of-sale terminal. BNPL appears as a payment method alongside UPI, credit cards, and wallets.

For online merchants, BNPL integration happens through the payment gateway. The gateway surfaces eligible BNPL options based on transaction value, merchant category, and customer eligibility signals already held by the BNPL provider. Offline, the integration happens via PoS systems or QR-based flows where UPI AutoPay is used to structure repayment.

The critical design principle here is friction reduction. Any additional step — a separate app redirect, a new KYC journey, a form — degrades conversion. Leading BNPL providers compete aggressively on checkout experience, particularly for returning users who have a pre-approved credit line.

- Step 2: Instant Credit Assessment

Once the customer selects BNPL, a real-time underwriting decision is triggered in the background. This is where the lending infrastructure does its most consequential work.

The credit assessment typically includes a soft bureau inquiry, which does not affect the customer's CIBIL score, combined with alternative data signals. These may include transaction history from the BNPL provider's own platform, bank statement analysis pulled via the account aggregator ecosystem, UPI transaction patterns, device intelligence, and telecom data. The output is a real-time credit decision: approved, declined, or approved for a reduced amount.

For new-to-credit customers, a significant portion of India's target demographic for BNPL, bureau data is thin or nonexistent. This is where alternative credit scoring models carry most of the underwriting weight, and where model risk concentrates. The accuracy of these models directly determines the delinquency profile of the BNPL book.

Approval timelines for returning users with established credit lines are typically sub-second. First-time users may face a slightly longer verification step involving Aadhaar-based e-KYC.

- Step 3: Payment Splitting and Merchant Settlement

Once approved, the BNPL provider pays the merchant in full, or near full net of the merchant discount rate, typically on a T+1 basis. This is a fundamental structural advantage for merchants: they receive immediate settlement regardless of the customer's repayment timeline.

The transaction is simultaneously converted into a repayment schedule for the customer. This may be a single deferred payment (pay in 30 days), a short-cycle split (three equal payments over six weeks), or a longer EMI structure (three to 24 months with or without interest).

In merchant-funded zero-cost EMI models, the merchant subsidizes the interest cost. The BNPL provider or lending partner charges the merchant a subvention fee, which is the commercial mechanism behind interest-free consumer credit. In consumer-funded models, the customer pays interest directly on the outstanding balance.

- Step 4: Repayment Cycle

Repayment is typically structured via UPI AutoPay e-mandates, which allow the BNPL provider to debit the customer's linked bank account on scheduled dates without requiring active payment initiation. This auto-debit mechanism is central to BNPL scalability, as manual repayment workflows at volume are operationally unsustainable.

NACH mandates are used for longer-tenure EMI products. The customer receives reminders via SMS and app notifications before each debit. Late payment fees apply if a debit fails due to insufficient funds.

For the BNPL provider, repayment behavior is the primary data signal for future credit limit adjustments. Consistent on-time repayment increases eligibility; missed payments trigger limit reductions and, under RBI digital lending guidelines, mandatory bureau reporting.

- Step 5: Delinquency and Collections Management

Repayment delinquency management is where the operational sophistication of a BNPL provider is most visibly tested. Early-stage delinquency (one to thirty days past due) is typically managed through automated digital nudges and self-cure mechanisms. Mid-stage delinquency triggers collections analytics workflows and outbound contact.

Collections infrastructure must comply with RBI fair practices guidelines, which prohibit coercive recovery tactics. Late-stage defaults escalate to credit bureau reporting and, in some cases, legal recovery under applicable lending agreements.

The full transaction flow can be summarized as: Customer → BNPL Provider (credit decision) → Merchant (settlement) → Customer (EMI repayment) → Bureau (reporting).

Modern fintechs operationalize each layer of this stack with dedicated infrastructure: underwriting APIs, collections dashboards, bureau reporting integrations, and fraud detection systems that operate continuously across the repayment lifecycle, not just at origination.

Key Business Models of BNPL in India

In India, BNPL is not a monolithic product. The commercial structure varies significantly depending on who funds the credit, who bears the default risk, and how the merchant is involved.

Merchant-Funded BNPL (Zero-Cost EMI)

This is the dominant model for high-ticket purchases in categories like consumer electronics, appliances, and furniture. The merchant pays a subvention fee to the lending partner, who then offers the customer an interest-free installment plan. The consumer pays exactly the product price; the interest subsidy is a merchant marketing cost.

ZestMoney built much of its early scale on this model, enabling structured no-cost EMI across major ecommerce platforms like Flipkart and Amazon. For merchants, the conversion economics typically justify the subvention expense. A 20 to 30% uplift in conversion on high-value items, combined with a higher average order value, usually more than offsets the cost. Payment gateway integrations with lending partners make this model available at scale without custom development for each merchant.

Consumer-Funded BNPL

For longer repayment tenures or higher-risk borrower segments, the consumer bears the interest cost. These products more closely resemble personal loans embedded at checkout. The lender earns interest income on the outstanding balance, and the product is disclosed as a formal loan under RBI digital lending guidelines, complete with a Key Fact Statement (KFS).

LazyPay and KreditBee operate meaningful books in this segment, offering credit lines to salaried professionals and gig workers who want structured consumer financing without the friction of a traditional bank loan application.

Card-Linked and Bank-Led BNPL

Banks and card networks have entered the BNPL space by converting existing credit card balances into installment products at the point of statement or at checkout. These products leverage existing credit bureau data and established customer relationships, offering lower underwriting risk but limited reach beyond the existing credit card base.

For embedded finance teams at banks, this is a high-margin extension of the existing credit infrastructure rather than a new lending vertical.

Wallet-Based and Direct Lending Models

Paytm Postpaid is the most widely recognized example of the wallet-linked model in India, where a revolving credit limit sits within the Paytm ecosystem and can be used across physical QR merchants, bill payments, and partner apps. Simpl operates a similar model within its own merchant partner network, emphasizing frictionless one-tap checkout with zero-cost billing cycles.

Others operate as standalone credit line products, disclosed as NBFCs, where the consumer has a reusable credit facility that refreshes with each repayment cycle. NBFC partnerships are central to this model, as the BNPL fintech provides the technology and distribution while the NBFC holds the lending license and manages the regulatory interface.

Why BNPL Is Growing Rapidly in India

The structural tailwinds behind BNPL in India are not cyclical. They reflect durable shifts in consumer behavior, credit access, and payment infrastructure.

India's credit card penetration remains below 5% of the adult population. The vast majority of digital payment users transact via UPI but have no formal revolving credit product. BNPL fills this gap, offering a credit experience that is natively digital, frictionless, and accessible to consumers who have never held a credit card.

The demographic profile of BNPL's heaviest users — millennials, Gen Z, gig workers, first-time earners in Tier 2 and Tier 3 cities — maps directly onto the segment that traditional credit has systematically underserved. These consumers have smartphones, digital identities, and transaction histories, but thin bureau files. BNPL underwriting models built on alternative data can extend credit to this segment in ways that bureau-dependent products cannot.

For merchants, competitive pressure on conversion rates is relentless. Checkout abandonment is directly correlated with payment friction and perceived affordability barriers. Offering BNPL at checkout is increasingly a baseline requirement for ecommerce merchants in categories above ₹3,000, not a differentiator but a table-stakes expectation.

The maturity of the UPI ecosystem has also lowered BNPL's operational cost significantly. UPI AutoPay makes repayment collection cheap and reliable. Account aggregator infrastructure enables bank statement analysis with customer consent. Aadhaar-based e-KYC makes digital onboarding possible without physical documentation. BNPL sits on top of a digital public infrastructure that makes it viable at a scale that would be impossible in markets without equivalent foundations.

Risks and Challenges of BNPL

The same design principles that make BNPL commercially successful also concentrate specific risks. For fintechs and merchants operating in this space, a clear-eyed risk framework is not optional.

Consumer Debt and Overspending

BNPL's primary consumer risk is the "phantom debt" problem: small ticket sizes reduce the psychological salience of borrowing. A consumer with four active BNPL lines across different merchants may not perceive them as debt until the aggregate monthly repayment burden becomes visible. Multiple BNPL obligations stacking against a fixed salary create delinquency risk that does not appear in any single credit bureau inquiry.

Repayment Delinquency

At the portfolio level, BNPL delinquency rates are structurally higher than secured lending because the product is unsecured, short-tenure, and targets borrower segments with limited credit history. Seasonal spikes in new-to-credit borrowers, particularly around festive seasons when BNPL volumes surge, can front-load default risk into future quarters.

Credit Risk Assessment Challenges

Alternative data models can underwrite new-to-credit consumers but carry inherent model risk. Behavioural signals such as UPI transaction frequency, app usage patterns, and telecom data are proxies for creditworthiness, not direct measures. Model drift, data quality issues, and adversarial behaviour (consumers gaming signals) are ongoing challenges that require continuous model recalibration.

Fraud and Identity Risks

BNPL is an attractive target for synthetic identity fraud, where fraudsters construct plausible digital identities using combinations of real and fabricated data to obtain credit lines they never intend to repay. Account takeover attacks, where legitimate user credentials are compromised to redirect repayments or extract credit, are also significant. Mule account networks, where multiple applications are submitted from the same device or IP address using different identities, require sophisticated transaction monitoring and device fingerprinting to detect.

Merchant fraud is an underappreciated risk: fake merchants processing transactions and absconding with BNPL settlement payouts represent a distribution-level vulnerability that payment orchestration controls must address.

Regulatory Scrutiny

BNPL has attracted consistent RBI attention precisely because of the risks outlined above. Regulatory scrutiny is not a transient phase; it is the new operating baseline. Compliance gaps create license risk for NBFCs and reputational risk for technology providers.

Merchant Dispute and Chargeback Complexity

When a customer disputes a purchase, citing non-delivery, defective goods, or unauthorized transaction, the triangular structure of BNPL (customer, merchant, BNPL provider) creates resolution complexity that pure payment products do not face. Chargeback workflows must be integrated with the lending agreement, and dispute resolution timelines affect both consumer credit bureau reporting and merchant settlement adjustments.

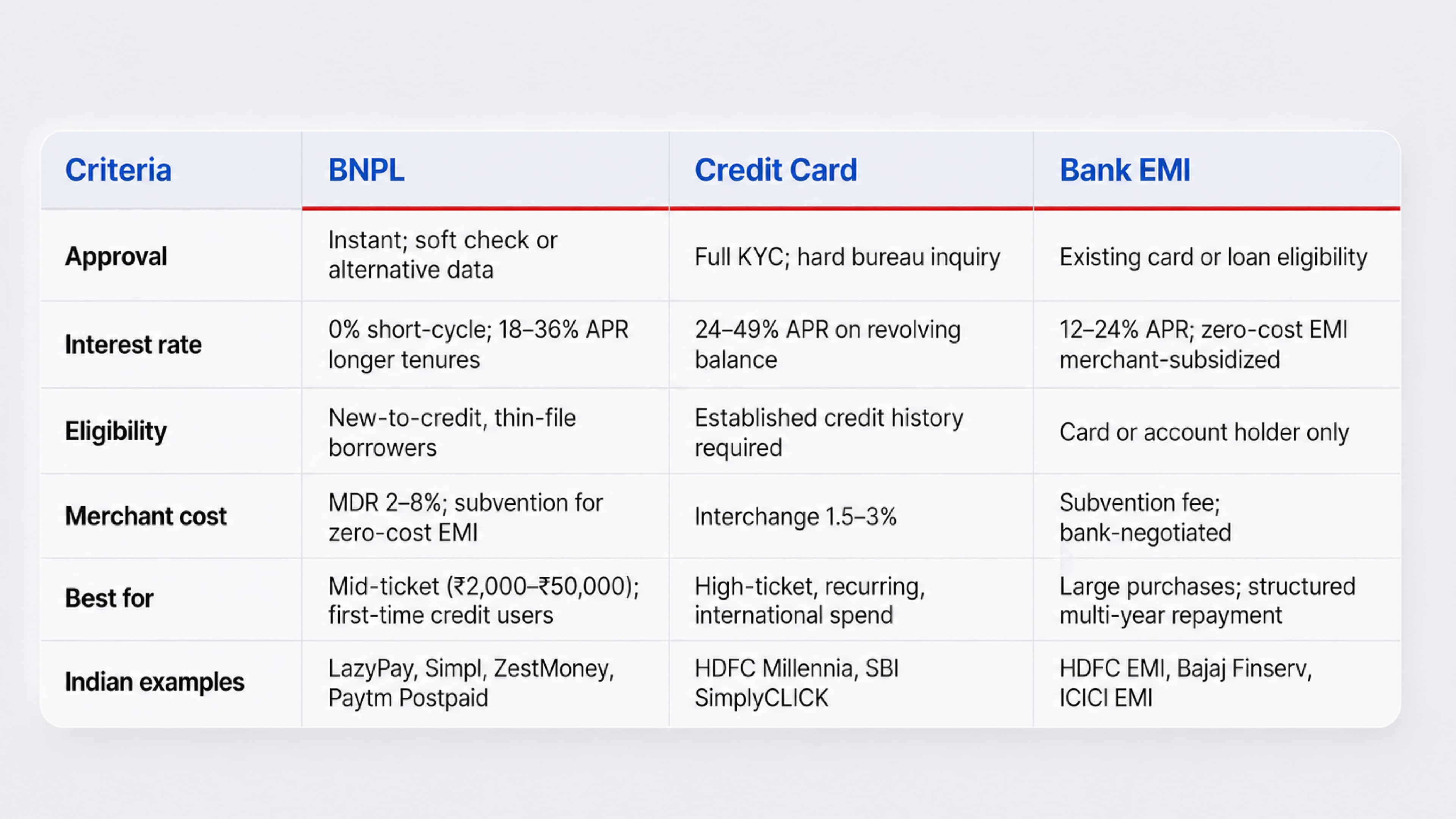

BNPL vs Credit Cards vs EMI — A Strategic Comparison

Understanding when BNPL makes sense, relative to credit cards and traditional EMI financing, is a strategic question that product managers and merchants must answer correctly to optimize both conversion and risk.

The table below captures the key operational and commercial differences across all three products.

Comparison of Buy Now Pay Later (BNPL), Credit Cards, and Bank EMI Options in India

A few strategic observations are worth drawing out from this comparison. First, BNPL and EMI are not substitutes — they serve different purchase values and different customer segments. Merchants who offer only one are leaving conversion on the table at both ends of the basket size range. Second, the bureau reporting parity that now exists under RBI guidelines means BNPL is no longer a "credit-score-free" product for consumers. This changes the risk calculus for both lenders and borrowers. Third, merchant economics across all three products are ultimately a function of conversion lift per rupee of subsidy or interchange paid — and that calculation is category-specific, not universal.

Regulatory Landscape of BNPL in India

The regulatory evolution of BNPL in India has moved from ambiguity to increasing formalization, and every operator in this space must understand the current framework and its operational implications.

The RBI's Digital Lending Guidelines, issued in 2022 and progressively clarified since, establish that any product that defers a payment obligation constitutes a loan. This requires every BNPL transaction to be backed by a Regulated Entity — a bank or NBFC — and disbursed directly from the lender's account to the borrower's account. Intermediary pool accounts, which many early BNPL providers used to pass credit through, are no longer permitted. This means fintechs that are not licensed NBFCs must operate through explicit lending partnerships rather than acting as de facto lenders.

KYC and AML obligations sit primarily with the lending partner, but technology providers and merchant aggregators cannot disclaim responsibility for the customer onboarding experience. Digital onboarding must use RBI-compliant e-KYC — Aadhaar OTP or video KYC — and the customer must receive a Key Fact Statement disclosing the total cost of credit, APR, processing fees, and late payment penalties before the transaction is confirmed.

The requirement for direct fund flow has significant implications for payment orchestration. BNPL providers that previously operated through wallet intermediaries have had to restructure their technical architecture to comply.

Consumer consent requirements have also tightened. Data collected during underwriting must be limited to what is necessary for credit assessment. The intrusive data access practices of some early digital lending apps, including harvesting contact lists, call logs, and photos, are explicitly prohibited.

From a fair lending standpoint, the RBI's Fair Practices Code requires transparent grievance redressal mechanisms, prohibition on coercive recovery practices, and clear disclosure of all fees. A cooling-off period of typically 24 hours must be provided after loan disbursement, during which the borrower can exit by returning the principal with minimal charges.

For compliance teams, the operational implication is clear: BNPL cannot be treated as a payments product with a thin lending wrapper. It requires the full compliance infrastructure of a digital lending operation, including KYC, AML, bureau reporting, fair practices disclosure, and an empowered grievance officer.

AI, Alternative Data, and Fraud Detection in BNPL

The underwriting and fraud prevention capabilities of modern BNPL infrastructure represent one of the most technically sophisticated layers in the Indian fintech stack.

AI and ML underwriting models process multiple data streams simultaneously to produce a real-time credit decision. Bank statement analysis, increasingly powered by account aggregator integrations where customers share bank data with explicit consent, enables income estimation, cash flow assessment, and spending pattern analysis without requiring physical salary slips. UPI transaction analysis reveals frequency, merchant category distribution, and repayment behavior from existing BNPL or loan obligations.

Device and telecom intelligence add a behavioral layer: the device used for the application, its risk score based on historical patterns, SIM age, and network operator provide signals that are difficult to spoof and highly predictive of fraud. Behavioral biometrics, specifically how a user interacts with the application interface, can flag robotic or scripted behavior associated with synthetic identity attacks.

Fraud detection systems in BNPL must operate across two distinct moments: at origination (identifying fraudulent applications before credit is extended) and throughout the repayment lifecycle (identifying account takeover or collusion fraud after credit is extended). Real-time transaction monitoring flags velocity anomalies such as multiple applications from the same device, rapid successive purchases after account opening, or repayment patterns inconsistent with stated income.

The account aggregator ecosystem is particularly valuable for BNPL underwriting because it provides consent-based, real-time financial data that is significantly harder to manipulate than self-declared information. As AA adoption grows and as data from multiple financial institutions becomes aggregable, the quality of BNPL underwriting decisions will improve materially.

The limits of alternative data models are equally important to acknowledge. Behavioral signals are proxies, not ground truth. Model bias, where certain demographics are systematically disadvantaged by proxy variables, is a regulatory risk that the RBI's fair lending framework is beginning to address. Data privacy obligations under India's Digital Personal Data Protection Act require explicit consent architecture for every data source used in underwriting.

The operational implication for fintech risk teams: AI underwriting must be paired with explainability infrastructure. A credit decision that cannot be explained to a regulator or a declined customer is a compliance exposure, not just a technical artifact.

Future Trends in BNPL and Embedded Finance

The next phase of BNPL in India will be defined less by user acquisition and more by infrastructure maturity, regulatory alignment, and convergence with the broader embedded finance stack.

Credit on UPI is the most consequential near-term development. The ability to link a pre-approved BNPL credit line to a UPI ID means that BNPL is no longer limited to partner merchant checkouts. A consumer can scan any UPI QR code at a local kirana, a petrol pump, or a medical clinic and pay using their credit limit, settling later. This expands BNPL's total addressable market from ecommerce to the entire UPI merchant network, which is now over 400 million endpoints.

Real-time underwriting will continue to improve as data infrastructure matures. The combination of account aggregator data, UPI transaction history, and device intelligence will enable credit decisions that are more accurate and faster than anything possible through bureau-only models. For fintech risk teams, this means the competitive advantage shifts from having access to data to having the model sophistication to use it correctly.

Cross-border BNPL is an emerging opportunity for Indian merchants selling to global consumers and for Indian consumers purchasing from international merchants. The operational complexity — regulatory alignment across jurisdictions, foreign exchange management, cross-border fraud patterns — is significant, but the market demand is clear as Indian ecommerce internationalizes.

Responsible lending frameworks will increasingly be a competitive differentiator rather than purely a compliance cost. As the RBI tightens oversight and as BNPL's consumer credit impact becomes more visible in bureau data, providers that have built responsible underwriting infrastructure, including genuine creditworthiness assessment, transparent disclosure, and proactive collections, will outperform those that optimized purely for volume.

Embedded finance convergence means that BNPL will increasingly cease to exist as a standalone product category. It will be a capability embedded within merchant checkout flows, banking apps, ecommerce platforms, and enterprise SaaS products, surfaced contextually when a financing need arises rather than marketed as a separate consumer product. Payment orchestration platforms and embedded finance infrastructure providers will be the enabling layer for this convergence.

Over the next three to five years, the distinction between a payment gateway, a lending platform, and a BNPL provider will continue to blur. The players that win will be those that can underwrite responsibly at scale, integrate seamlessly into any payment environment, and operate within a compliance framework robust enough to survive increasing regulatory scrutiny.

Frequently Asked Questions

What is BNPL?

Buy Now Pay Later is a short-term financing product that allows a consumer to complete a purchase immediately and repay the cost, either in a lump sum after a grace period or in structured installments, over a defined timeframe. Legally, it is classified as an unsecured consumer loan under RBI's Digital Lending Guidelines and must be backed by a regulated entity such as a bank or NBFC.

How does Buy Now Pay Later work in India?

When a customer selects BNPL at checkout, the BNPL provider triggers a real-time credit assessment using bureau data, alternative data sources, and behavioral signals. If approved, the provider pays the merchant immediately and creates a repayment schedule for the customer, typically via UPI AutoPay or NACH mandate. The customer repays in installments over an agreed period, with or without interest depending on the product structure.

Is BNPL different from a credit card?

Yes, in several important ways. Credit cards require an established bureau history and full KYC for approval; BNPL can serve thin-file borrowers using alternative data. Credit cards operate on revolving credit with interest charged on unpaid balances; short-cycle BNPL is typically interest-free within the grace period. BNPL approval is near-instant and embedded at checkout; credit card applications are processed separately. Both create consumer credit obligations that affect bureau profiles when reported.

Does BNPL affect credit scores?

Under current RBI digital lending guidelines, BNPL transactions must be reported to credit bureaus as short-term personal loans. Timely repayments can build a positive credit history; missed payments negatively affect CIBIL scores. Historically, some providers did not report consistently, but mandatory reporting requirements have closed this gap.

How is BNPL regulated in India?

BNPL is regulated under the RBI's Digital Lending Guidelines, which require that all BNPL products be backed by a Regulated Entity (bank or NBFC), that loan disbursements flow directly from lender to borrower without intermediary pool accounts, and that consumers receive a Key Fact Statement disclosing total cost of credit before the transaction is confirmed. KYC obligations, AML compliance, bureau reporting, and fair practices disclosures are mandatory.

What are the risks of BNPL for businesses and consumers?

For consumers, the primary risks are debt accumulation across multiple BNPL lines, late payment penalties that can significantly increase the effective cost of credit, and the behavioral tendency to underestimate deferred payment obligations. For businesses, both merchants and fintech providers, the risks include credit defaults from thin-file borrowers, synthetic identity fraud, chargeback complexity, increasing regulatory compliance costs, and reputational exposure if collections practices fall outside RBI fair lending guidelines.

Conclusion

BNPL's trajectory in India is not in question. The structural drivers — low credit card penetration, UPI-native consumers, a massive new-to-credit demographic, and merchant pressure on conversion — will sustain growth for the foreseeable future. What is in question is whether the ecosystem matures responsibly.

The market is moving from a period of rapid, largely unregulated expansion toward one of regulatory formalization and operational accountability. The RBI has made clear that deferred payment products are loans, that they require regulated entity backing, and that consumer protection obligations are non-negotiable. For fintech founders and payment operations leaders, this is not a headwind; it is a clarifying signal about where durable competitive advantage lies.

The operators that will define India's BNPL market over the next decade are those that treat underwriting as a precision capability rather than a throughput function, that build fraud detection systems capable of operating across the full repayment lifecycle, and that design their compliance infrastructure as a strategic asset rather than a cost center.

Modern fintechs and merchants need real-time, compliant, and data-driven payment risk infrastructure to scale BNPL safely in a regulated environment. The checkout experience is only as sustainable as the underwriting and risk management stack that sits behind it.

Building a BNPL integration or scaling a digital lending product? Speak to IDfy's payments and risk infrastructure specialists to understand how compliant, real-time underwriting can reduce delinquency and accelerate growth.

Explore the 2026 payment fraud landscape in India. Learn the most common types of payment fraud, the emerging fraud trends, and how to build a future-ready fraud prevention strategy.