Types of Credit Risk in Banking and Lending: India Guide (2026)

Date Published

India's credit ecosystem has undergone a structural transformation over the past five years. The rapid expansion of digital lending, the surge in unsecured retail credit, the proliferation of NBFC co-lending arrangements, and the increasing regulatory focus on portfolio quality have collectively raised the stakes for credit risk professionals. Where risk management once meant managing a single book of term loans and working capital facilities, it now spans embedded finance partnerships, buy-now-pay-later products, MSME cash flow lending, and cross-border treasury operations.

Against this backdrop, understanding the distinct categories of credit risk is no longer foundational knowledge reserved for analysts. It is a strategic imperative for CROs, credit policy teams, underwriting leaders, and fintech operators who must manage exposure across increasingly complex and interconnected portfolios.

This guide defines the six main types of credit risk, explains their operational and regulatory relevance in India's lending environment, and outlines how banks, NBFCs, and digital lenders classify, monitor, and mitigate each category.

What is Credit Risk?

Credit risk refers to the probability that a borrower, counterparty, or issuer fails to meet its financial obligations as agreed, resulting in a loss for the lending institution or investor.

In practical terms, credit risk is the foundational risk category for any institution that extends credit, invests in debt instruments, or transacts with counterparties in financial markets. It affects underwriting decisions, pricing of loans and bonds, capital allocation, provisioning requirements, and collection strategy.

For Indian banks and NBFCs, credit risk management covers a wide terrain. It includes assessing the likelihood that a retail borrower defaults on a personal loan, determining whether a mid-market business can service its working capital facility, estimating the exposure to a settlement counterparty in interbank transactions, and monitoring portfolio concentration across sectors and geographies.

Credit risk is distinct from market risk and operational risk, though the three interact in complex ways during periods of economic stress. A deeper treatment of credit risk modelling approaches, including probability of default estimation, loss given default, and exposure at default, is covered separately in our guide on credit risk modelling frameworks.

The 6 Main Types of Credit Risk

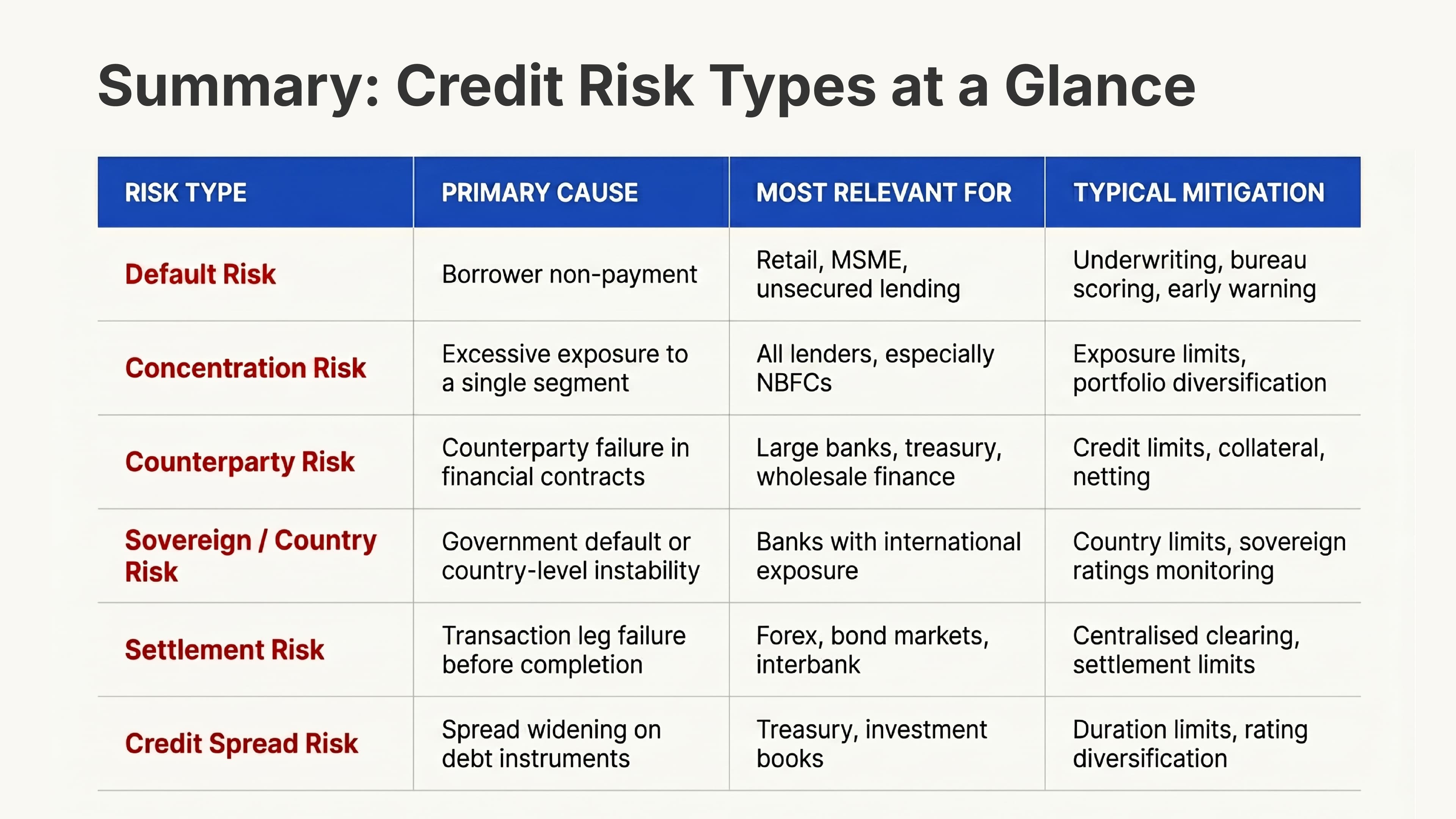

Default Risk

Default risk is the most direct and widely understood form of credit risk. It is the probability that a borrower fails to make scheduled repayments, either partially or entirely, resulting in the lender recognising a loss.

In India's retail lending market, default risk is the dominant credit concern for most NBFCs and digital lenders. Personal loan delinquencies, missed EMI payments on consumer durables, and cashflow disruptions in MSME lending all represent manifestations of default risk at different points in the credit lifecycle.

The consequences are significant. When borrowers default, accounts are classified as non-performing assets according to RBI's asset classification norms. Lenders must then set aside provisions according to the applicable provisioning framework, which varies by loan category, collateral status, and days past due. Persistent NPA accretion erodes net interest margins, constrains capital deployment, and invites regulatory scrutiny.

Operational implications: Default risk management depends on the quality of underwriting at origination. Bureau-based credit scoring, income verification, bank statement analysis, and increasingly, alternative data signals from Account Aggregator-consented financial data are all used to estimate the probability of default before disbursement. Post-disbursement, early warning systems that track payment behaviour, utilisation patterns, and bureau updates provide the first line of defence.

For unsecured digital lenders, default risk is amplified by the absence of collateral recovery options. The margin for underwriting error is narrow, and vintage-based monitoring of cohort performance is critical to detecting deterioration early.

Concentration Risk

Concentration risk arises when a lender's portfolio is disproportionately exposed to a single borrower, sector, geography, or product type. When stress hits that concentrated segment, the impact on portfolio quality is amplified beyond what a diversified book would experience.

The RBI has long addressed concentration risk through prudential exposure norms. For scheduled commercial banks, exposure to a single borrower is capped at 20% of eligible capital base, and exposure to a connected group of entities is capped at 25%, with provisions for infrastructure-related exceptions. These limits are designed to prevent idiosyncratic borrower stress from threatening institutional solvency.

In practice, concentration risk in Indian lending takes several forms:

- Sectoral concentration: Lenders heavily exposed to real estate, microfinance, or unsecured retail face amplified risk when those sectors experience cyclical stress. The stress events in the microfinance sector in 2024 and 2025, driven by over-indebtedness among borrowers and collection disruptions in specific states, illustrate how sectoral concentration can compress credit quality across multiple lenders simultaneously.

- Geographic concentration: NBFCs and MFIs with high exposure in a single state or region face elevated risk from localised events, policy changes, or collection environment deterioration.

- Borrower concentration: In commercial and wholesale lending, significant exposure to a handful of large borrowers creates binary risk: if one large account deteriorates, the portfolio impact is disproportionate.

Operational implications: Lenders manage concentration risk through exposure limits built into credit policy, periodic portfolio segmentation analysis, and sectoral caps approved at board level. Stress testing should model scenarios where a single sector or geography experiences simultaneous deterioration.

For vehicle finance NBFCs and MSME-focused lenders, geographic concentration is often a product of distribution strategy. As they scale, proactive portfolio rebalancing through co-lending and assignment becomes both a business and risk management tool.

Counterparty Risk

Counterparty credit risk refers to the possibility that the other party in a financial transaction fails to fulfil its obligations before the final settlement of the transaction. This is distinct from default risk in retail lending: counterparty risk typically applies to treasury operations, interbank markets, derivatives, and trade finance.

For larger Indian banks operating in institutional financial markets, counterparty risk is a daily operational reality. A bank entering into an interest rate swap, a foreign exchange forward contract, or a repo transaction is exposed to the risk that its counterparty defaults or becomes unable to perform before the contract settles.

The exposure is often bilateral and dynamic: as the mark-to-market value of a derivative position shifts, the counterparty exposure changes correspondingly. This is referred to as current exposure, and prudent treasury desks track it continuously alongside potential future exposure metrics.

Operational implications: Counterparty risk is managed through credit limits assigned to each counterparty based on creditworthiness, collateral and margin requirements (especially under ISDA master agreements for OTC derivatives), netting arrangements, and regular counterparty credit reviews.

While counterparty risk is less relevant for smaller retail NBFCs, it becomes material as institutions grow their treasury books, participate in co-lending arrangements, and engage in securitisation transactions where counterparty performance affects cash flow timing.

Country and Sovereign Risk

Sovereign risk is the probability that a national government defaults on its obligations or takes actions that impair the ability of borrowers within its jurisdiction to service external debt. Country risk is the broader category that includes political instability, foreign exchange controls, expropriation risk, and regulatory unpredictability that can affect cross-border credit exposure.

For Indian banks with international operations, branches in Southeast Asia and the Middle East, or export finance portfolios, sovereign and country risk is a structured risk management discipline. Exposure to sovereign bonds issued by governments with deteriorating fiscal positions, lending to entities in countries with currency instability, or interbank credit lines extended to banks in emerging markets all carry sovereign risk components.

India's own sovereign risk profile has remained relatively stable, supported by robust foreign exchange reserves, a large domestic savings base, and RBI's proactive management of external sector vulnerabilities. However, Indian lenders extending trade finance facilities to exporters operating in markets with elevated country risk must build that risk into their credit assessments.

Operational implications: Country risk is typically managed through country exposure limits, haircuts on sovereign-rated collateral from lower-rated jurisdictions, and ongoing monitoring of political, fiscal, and currency conditions in markets where exposure exists.

Settlement Risk

Settlement risk arises when one party to a financial transaction discharges its obligation while the counterparty fails to deliver on its side of the transaction, resulting in a loss. It is sometimes called Herstatt risk, named after the German bank whose failure in 1974 left counterparties exposed to uncompleted foreign exchange settlements.

In India's financial markets, settlement risk is most directly relevant to:

- Foreign exchange transactions: Where payment legs occur across different time zones and settlement systems, there is a window during which one leg may be completed while the other fails.

- Government securities and bond market transactions: Settlement in the Clearing Corporation of India (CCIL) infrastructure reduces but does not eliminate settlement risk for non-cleared transactions.

- Interbank and money market operations: Short-duration transactions in the call money market and certificate of deposit space carry settlement timing risk.

- Trade finance: Letters of credit and documentary collections involve timing gaps between document presentation and payment that create settlement exposure.

Operational implications: The Reserve Bank of India has progressively strengthened payment and settlement infrastructure through RTGS, CCIL-mandated central clearing for government securities and forex, and payment system regulations under the Payment and Settlement Systems Act. These reduce systemic settlement risk. However, bilateral settlement arrangements in non-cleared products still require internal management through settlement limits and netting agreements.

Credit Spread Risk

Credit spread risk is the risk that the value of a debt instrument declines due to a widening of the credit spread, which is the yield premium demanded by investors to hold that instrument over a risk-free benchmark. Unlike default risk, credit spread risk can materialise even when no default occurs: a deterioration in perceived creditworthiness causes the market price of the bond to fall, generating mark-to-market losses.

For Indian banks and NBFCs holding corporate bond portfolios, non-SLR investments, and structured credit instruments, credit spread risk is an investment book concern that sits at the intersection of credit and market risk.

When macroeconomic conditions tighten or a particular sector comes under stress, spreads on debt instruments issued by entities in that sector may widen sharply. A treasury portfolio concentrated in a single rating category or sector is exposed to correlated spread movements.

Operational implications: Credit spread risk is managed through duration limits on credit portfolios, rating-based concentration limits in the investment book, mark-to-market monitoring, and stress testing of spread movements under adverse scenarios.

Overview of common credit risks affecting banks, NBFCs, lenders, and investment firms.

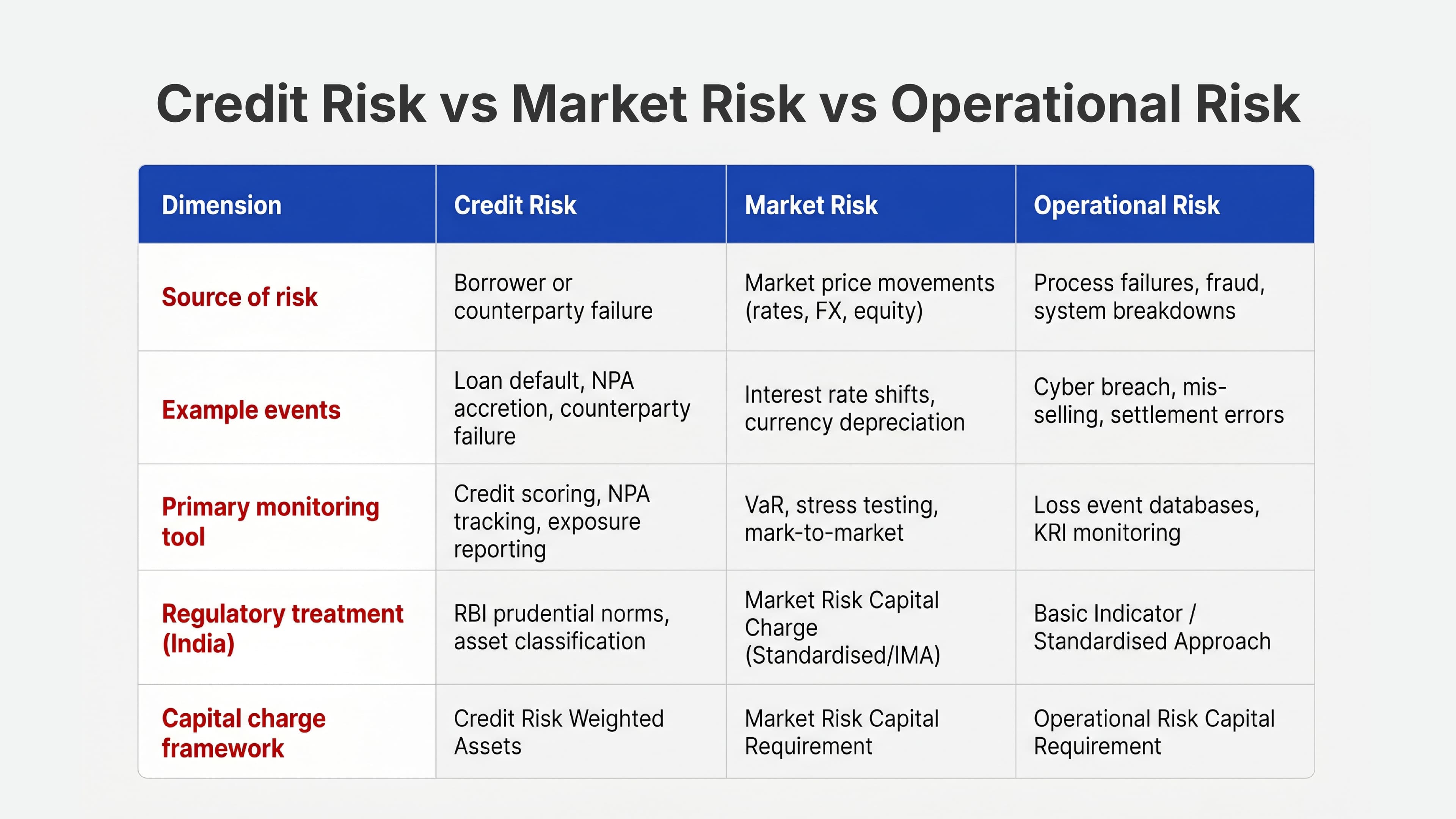

Credit Risk vs Market Risk vs Operational Risk

Risk frameworks in banking separate credit, market, and operational risk because they have different sources, different measurement methodologies, and different capital treatment under Basel III and RBI's capital adequacy guidelines.

Understanding these distinctions matters operationally: it determines which risk function owns the exposure, how it is measured, what capital is allocated against it, and how regulators expect it to be reported.

Understanding the differences between credit risk, market risk, and operational risk.

A critical nuance: the three risk types are not independent. A period of sharp interest rate increases (market risk event) can trigger borrower stress and NPA accretion (credit risk outcome). A fraud-driven operational failure can generate credit losses. Risk governance frameworks must account for these interactions, particularly in stress testing.

Which Types of Credit Risk Matter Most for Indian NBFCs?

NBFCs operating in India face a credit risk profile that differs meaningfully from that of large scheduled commercial banks. The differences stem from their funding structure, borrower segments, geographic footprints, and regulatory environment.

Default risk is the central concern. Most Indian NBFCs are concentrated in retail unsecured lending, vehicle finance, microfinance, or MSME lending. All of these segments are sensitive to income volatility, employment disruption, and collection environment changes. Unlike secured retail lenders who can recover collateral, unsecured NBFCs must price and monitor default risk with precision.

Concentration risk is structurally elevated. Many NBFCs built their books in specific geographies or segments where they had distribution advantages. As a result, their portfolios carry meaningful sectoral and geographic concentration. When those segments face stress, the absence of diversification amplifies the impact.

Model and behavioural risk is growing. Fintech-oriented NBFCs that rely on alternative data and machine learning-based underwriting models carry a category of risk not fully captured in traditional frameworks: the risk that models trained on benign credit conditions underperform when the macroeconomic environment shifts. This is sometimes treated as a subset of operational risk but has direct credit risk consequences.

Co-lending and assignment exposure. As NBFCs scale through bank co-lending partnerships and portfolio assignment transactions, they take on concentration of a different kind: operational dependence on a limited number of bank partners and exposure to counterparty risk if those arrangements are restructured.

Segment-specific observations:

- BNPL and short-tenure digital lenders: Highly exposed to default risk from thin-file borrowers; bureau depth is limited, and behavioural signals matter more than traditional credit scores.

- Vehicle finance NBFCs: Concentration risk in specific asset classes (commercial vehicles, two-wheelers) and geographies is a primary concern; collateral quality and recovery infrastructure matter.

- MSME lenders: Cash flow volatility among small businesses makes default risk assessment more complex; overdependence on GST-linked income proxies creates model risk when those proxies become less reliable.

How Lenders Classify and Monitor Each Risk Type

Effective credit risk management requires more than classifying risk at origination. It demands continuous monitoring across the credit lifecycle, with escalation mechanisms that surface emerging stress before it becomes portfolio-level deterioration.

Portfolio segmentation is the starting point. Lenders segment their books by product type, borrower segment, geography, vintage (origination cohort), and risk grade. Each segment is monitored independently so that stress in one segment is visible before it contaminates the aggregate.

Monitoring workflow for a mid-size NBFC:

- Origination: Credit bureau pull, income verification, fraud check, underwriting model score, credit policy check against concentration limits.

- Early delinquency tracking (Days 1 to 30 past due): Automated triggers for collection outreach; cohort performance tracked against expected vintage curves.

- Early Warning System (EWS) signals: Bureau updates, bank account activity (via Account Aggregator), GST filing status, legal alerts, and social signal monitoring for MSME borrowers.

- Portfolio review (monthly/quarterly): NPA movement, provision coverage ratio, sectoral and geographic concentration reports, vintage performance versus underwriting assumptions.

- Stress testing (quarterly/semi-annual): Adverse macro scenarios applied to the portfolio to estimate incremental NPA and provisioning requirements.

- Board-level credit and risk committee review: Concentration limit compliance, NPA trajectory, capital adequacy, and forward-looking risk indicators.

Analytics and AI systems are increasingly embedded across this workflow, automating data aggregation, anomaly detection, and early warning flag generation. The institutional value of these systems lies not in automation for its own sake but in the speed at which risk signals surface to decision-makers.

Regulatory View: RBI Guidelines on Credit Risk Categories

The Reserve Bank of India has a comprehensive framework governing credit risk management for both banks and NBFCs, grounded in Basel III principles and adapted to India's lending and financial market structure.

Key regulatory dimensions:

- Prudential exposure norms: RBI limits single-borrower and group exposure to prevent excessive concentration in the banking system. For banks, these are expressed as percentages of eligible capital base. NBFCs have analogous concentration guidelines under the Scale-Based Regulation (SBR) framework.

- Asset classification and provisioning: RBI's asset classification norms define when a loan becomes a Special Mention Account (SMA-0, SMA-1, SMA-2) and when it is classified as a Non-Performing Asset. Provisioning rates escalate as accounts move from Sub-Standard to Doubtful to Loss categories. These norms apply across all regulated entities.

- Basel III capital adequacy: Scheduled commercial banks are required to maintain minimum capital ratios under RBI's Basel III guidelines, with credit risk-weighted assets forming the largest component of total RWA for most banks. The standardised approach to credit risk assigns risk weights to different asset classes based on counterparty type and rating.

- Stress testing expectations: RBI expects banks and systemically important NBFCs to conduct regular stress testing across credit, market, and liquidity risk dimensions, with results used to assess capital adequacy and inform risk appetite.

- Unsecured retail and digital lending scrutiny: In recent years, the RBI has signalled increasing supervisory attention to the growth of unsecured retail credit and digital lending. Risk weight increases on consumer credit and bank credit to NBFCs (announced in late 2023 and carried forward into supervisory posture in subsequent periods) reflect concern about concentration of risk in high-growth, thin-margin unsecured lending.

- Governance expectations: RBI's guidelines on credit risk management emphasise board-approved risk appetite statements, independent credit risk functions separate from business, and documented concentration limits with regular compliance monitoring.

Conclusion

The credit risk landscape facing Indian banks, NBFCs, and digital lenders in 2026 is more layered than it has ever been. Default risk remains the dominant concern for retail and MSME lenders. Concentration risk is structurally embedded in many NBFC business models and requires active portfolio management to contain. Counterparty, settlement, sovereign, and credit spread risks have historically been the domain of large banks but are increasingly relevant as NBFCs scale, raise market-rate debt, and engage in more complex balance sheet transactions.

What ties these categories together is the need for portfolio-level visibility. Individual loan decisions matter, but the shape of the portfolio, how it responds to stress, where exposures cluster, and how quickly risk signals escalate are what determine whether an institution navigates a credit cycle or is defined by it.

As digital lending ecosystems scale, credit risk management increasingly depends on integrated identity, fraud, monitoring, and underwriting infrastructure. The institutions that build that infrastructure thoughtfully, aligned to regulatory expectations and grounded in operational discipline, will be better positioned to manage the credit cycles that inevitably follow periods of rapid credit growth.

Frequently Asked Questions

What are the main types of credit risk?

The six main types of credit risk are: default risk (borrower non-payment), concentration risk (overexposure to a single segment), counterparty risk (counterparty failure in financial contracts), sovereign or country risk (government or jurisdiction-level default risk), settlement risk (transaction leg failure before completion), and credit spread risk (mark-to-market losses from spread widening on debt instruments).

What is default risk in banking?

Default risk is the probability that a borrower fails to make scheduled loan repayments, resulting in the lender recognising a loss. It is the most common form of credit risk in retail and commercial lending. In India's banking system, persistent default leads to NPA classification under RBI's asset classification norms, triggering provisioning requirements and capital impact.

What is counterparty credit risk?

Counterparty credit risk is the risk that the other party in a financial contract, such as a derivatives trade, repo agreement, or interbank transaction, fails to fulfil its obligations before final settlement. It is most relevant for large banks operating in treasury and institutional markets and is managed through counterparty credit limits, collateral arrangements, and central clearing.

What is concentration risk?

Concentration risk is the risk of losses arising from excessive exposure to a single borrower, sector, geography, or product type. When the concentrated segment experiences stress, the portfolio impact is amplified. RBI addresses concentration risk through single-borrower and group exposure limits for banks, and similar guidelines apply to NBFCs under the Scale-Based Regulation framework.

What is the difference between market risk and credit risk?

Credit risk arises from the failure of a borrower or counterparty to meet financial obligations. Market risk arises from movements in market prices, including interest rates, foreign exchange rates, and equity prices. While distinct in origin, they interact: a market risk event such as a sharp interest rate increase can trigger credit stress by impairing borrower repayment capacity. Under Basel III, they carry separate capital charges.

Why is concentration risk important for NBFCs?

Many Indian NBFCs have built portfolios concentrated in specific sectors (microfinance, vehicle finance, MSME) and geographies. This concentration creates amplified risk during sector-specific or region-specific stress events. Regulatory frameworks increasingly require NBFCs to monitor and manage concentration actively, and lenders that fail to diversify are more vulnerable to rapid NPA accretion during downturns.

Explore how leading NBFCs and digital lenders are building portfolio monitoring and early warning capabilities to manage credit risk at scale with IDfy.

A complete guide to credit underwriting, process, benefits, challenges, best software for underwriting, and real-world use cases for lenders.

A practical guide to credit risk management in India — types, RBI framework, 5-step process, tools, and NBFC-specific challenges.

Understand credit risk assessment models, PD/LGD/EAD, scorecards, and the lending risk process used by Indian banks and NBFCs.