Cross-Border Payments Explained: A Complete Guide for Indian Businesses (2026)

Date Published

India's integration into the global digital economy is no longer aspirational — it is operational. SaaS companies in Bengaluru are billing Fortune 500 clients in the United States. Freelancers in Tier 2 cities are receiving project payments from European agencies. Export manufacturers in Gujarat are settling invoices with buyers across the Middle East and Southeast Asia. And D2C brands are shipping to international consumers through global marketplaces.

This expansion has made cross-border payment infrastructure one of the most strategically consequential layers of India's financial system. The ability to collect, convert, and settle international payments efficiently is no longer a back-office concern. It directly affects revenue recognition, working capital cycles, customer experience, and regulatory standing.

At the same time, the RBI has significantly raised its compliance expectations. Licensing requirements for payment aggregators handling cross-border transactions have been formalized. AML checks, KYC verification, and transaction monitoring are now non-negotiable components of any international payment stack. For Indian businesses and fintechs operating globally, the question is no longer whether to invest in compliance infrastructure — it is how to build it intelligently.

This guide provides a comprehensive operational and regulatory view of cross-border payments in India in 2026.

What Are Cross-Border Payments?

Cross-border payments are financial transactions in which the payer and payee are located in different countries. They involve the movement of funds across currency zones, regulatory jurisdictions, and banking systems.

In practical terms, this covers a wide range of transaction types:

- A SaaS startup charging a US client in USD and receiving settlement in INR

- A freelancer receiving project-based payments from a European client

- An exporter receiving foreign currency against an invoice for physical goods

- An international marketplace routing payments to Indian sellers from global buyers

- A business paying an overseas supplier or service provider

What distinguishes cross-border payments from domestic transactions is not just geography. It is the additional complexity introduced by foreign exchange conversion, multi-jurisdiction regulatory compliance, multiple intermediary institutions, and longer settlement timelines.

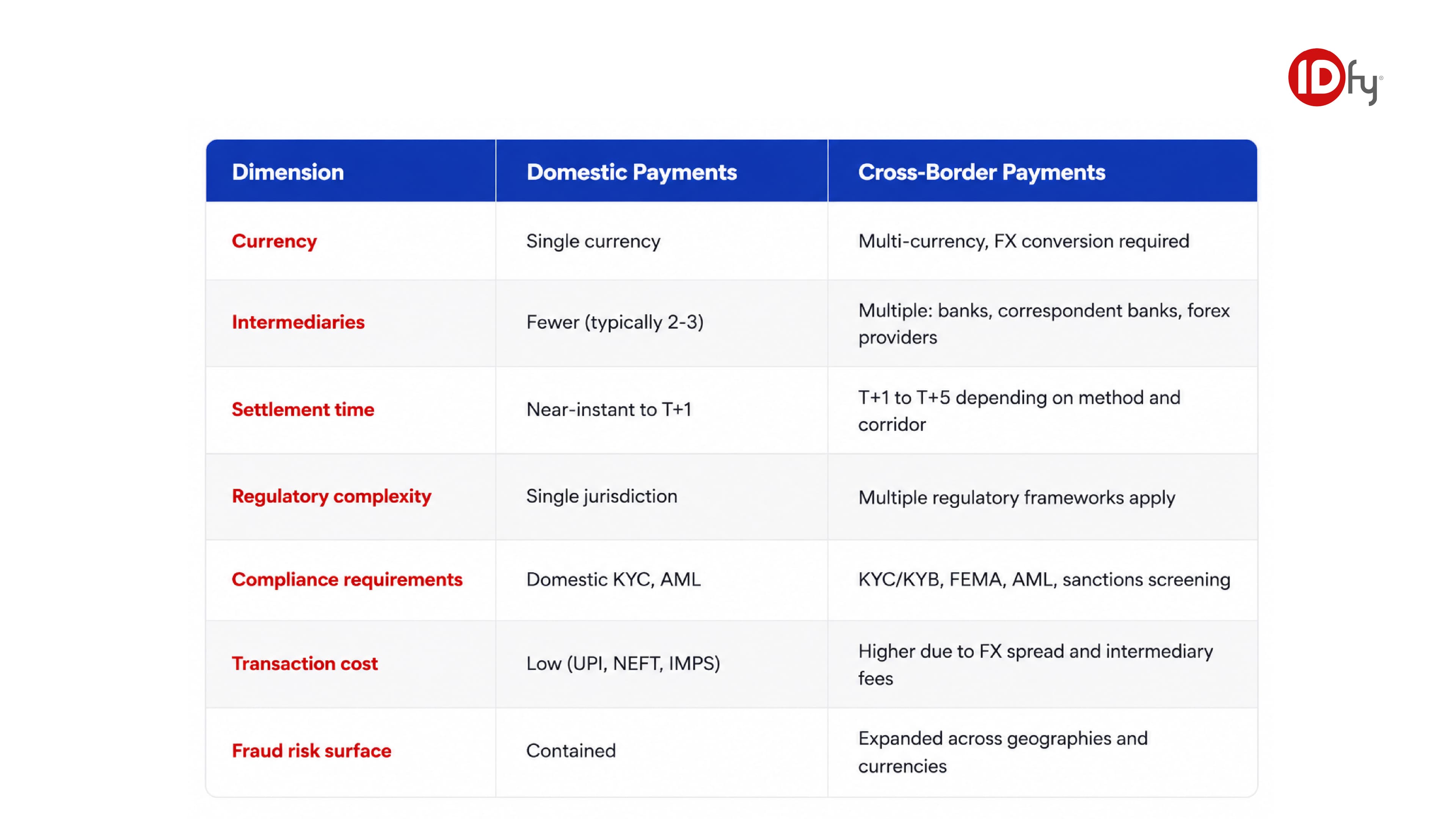

Domestic vs Cross Border Payments: Key Differences Explained for Indian Financial Institutions

The compliance and operational layers involved in cross-border transactions are fundamentally different from domestic payment rails. This distinction matters enormously when designing payment infrastructure or scaling global operations.

Why Cross-Border Payments Matter for Indian Businesses

India's services exports crossed USD 340 billion in FY24. Software and IT services alone account for a significant share. Independent research consistently points to India as one of the largest sources of digital services exports globally.

Several structural trends are converging to make cross-border payment capability mission-critical for Indian businesses.

Global SaaS expansion

Indian SaaS companies targeting enterprise clients abroad need payment infrastructure that can handle multi-currency billing, automated reconciliation, and country-specific compliance requirements.

The remote work economy

India is among the top countries for cross-border freelance income. Platforms like Upwork, Toptal, and direct client relationships generate sustained inward remittance flows that require efficient, compliant payment channels.

International ecommerce

D2C brands and marketplace sellers are increasingly reaching global consumers. Collecting payments across card networks, digital wallets, and local payment methods requires gateway infrastructure designed for international acquiring.

Cross-border B2B services

Consulting, legal, creative, and technology services firms are billing international clients with varying payment preferences, invoice currencies, and settlement requirements.

For Indian businesses, the operational quality of cross-border payment infrastructure affects how quickly funds arrive, how much is lost to FX spreads and fees, and how confidently they can scale globally without compliance risk.

Faster settlement cycles and lower transaction costs are not just operational metrics. They directly improve working capital efficiency. For a SaaS company collecting USD 500K per month from international clients, even a 0.5% improvement in the effective FX rate translates to USD 2,500 per month in recovered value.

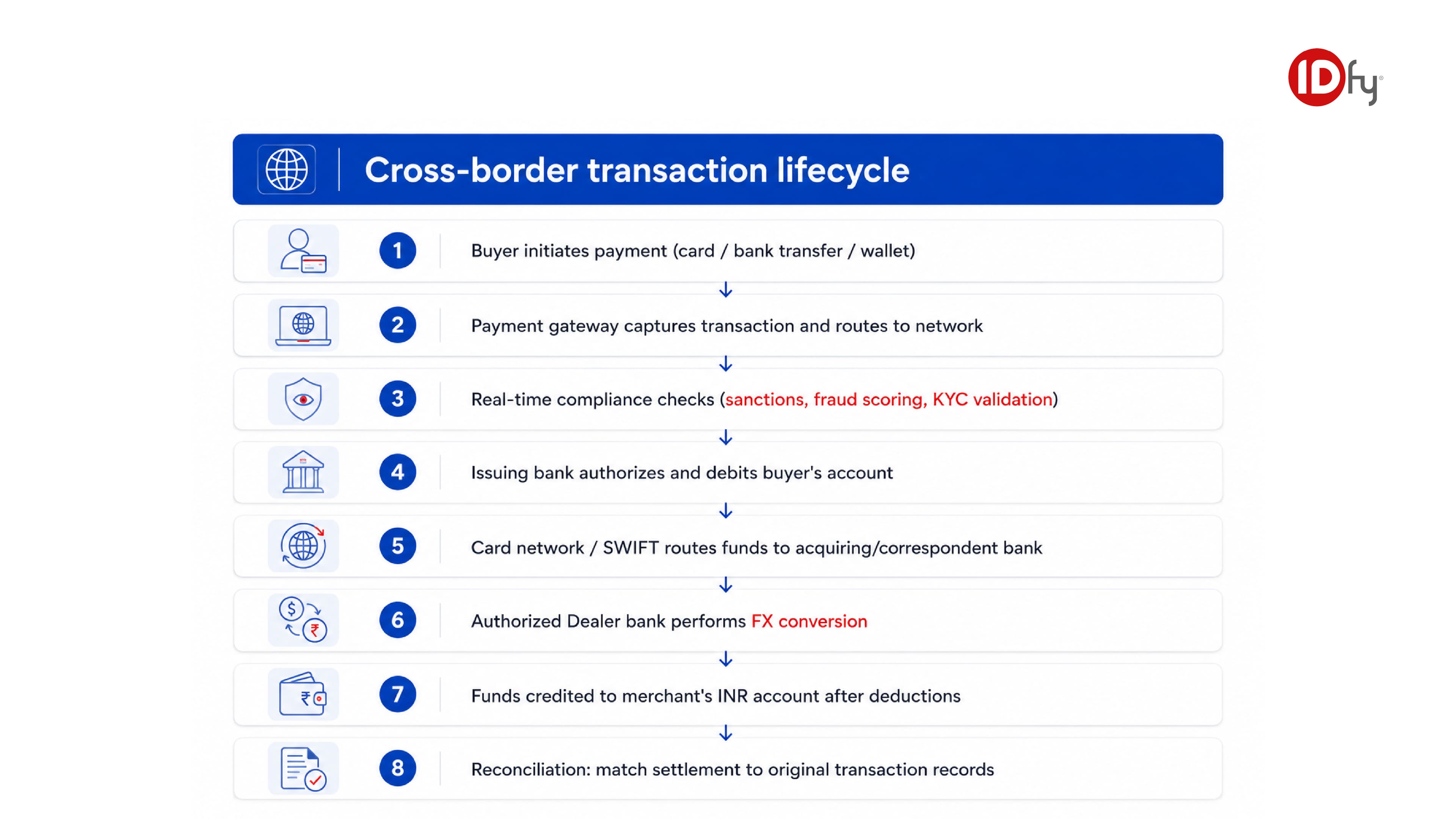

How Cross-Border Payments Work: Step-by-Step

Understanding the operational mechanics of a cross-border transaction helps businesses identify where delays, costs, and compliance gaps typically emerge.

A step-by-step flowchart showing the lifecycle of a corss-border transaction in India, from payment initiation and compliance screening to SWIFT routing, FX conversion, settlement, and reconciliation.

Step 1: Payment Initiation

The transaction begins when a buyer initiates a payment — by entering card details on a checkout page, authorizing a wire transfer, or confirming a wallet-based payment. On the merchant side, this is preceded by invoice generation, payment link creation, or a checkout experience configured for international buyers.

At initiation, the payment gateway captures transaction parameters: currency, amount, buyer details, and merchant identifier. Merchant onboarding with the payment provider determines what payment methods are available, which currencies are accepted, and what compliance checks are pre-configured.

Step 2: Payment Processing and Routing

Once the transaction is initiated, the payment gateway or processor routes it through the appropriate network. For card-based payments, this involves the card scheme network (Visa, Mastercard) connecting the issuing bank (buyer's bank) to the acquiring bank (merchant's bank). For bank transfers, messaging protocols like SWIFT carry payment instructions across correspondent banking networks.

During processing, the payment processor performs real-time compliance checks: sanctions screening against lists maintained by OFAC, UN, and EU regulators; velocity checks to detect unusual transaction patterns; and fraud scoring based on device, behavioral, and transactional signals.

Step 3: Currency Conversion

If the transaction currency differs from the settlement currency, foreign exchange conversion is applied. In India, authorized dealer (AD) banks — licensed by the RBI to deal in foreign exchange — handle this conversion. The exchange rate applied includes a spread above the interbank rate, which represents a cost component for the merchant.

For high-volume businesses, treasury management at this stage becomes important. FX hedging strategies, dynamic currency conversion options, and choice of currency settlement windows can materially affect effective revenue.

Step 4: Settlement in INR

After conversion, the funds are settled into the merchant's bank account in INR. This involves the movement of funds through Nostro and Vostro accounts — correspondent banking accounts maintained by Indian banks in foreign financial institutions and vice versa.

Settlement timelines typically range from T+1 to T+5 depending on the payment method, the originating country, and the intermediary banking chain. Reconciliation workflows must account for these timelines, currency conversion records, and fee deductions to accurately match settlements to individual transactions.

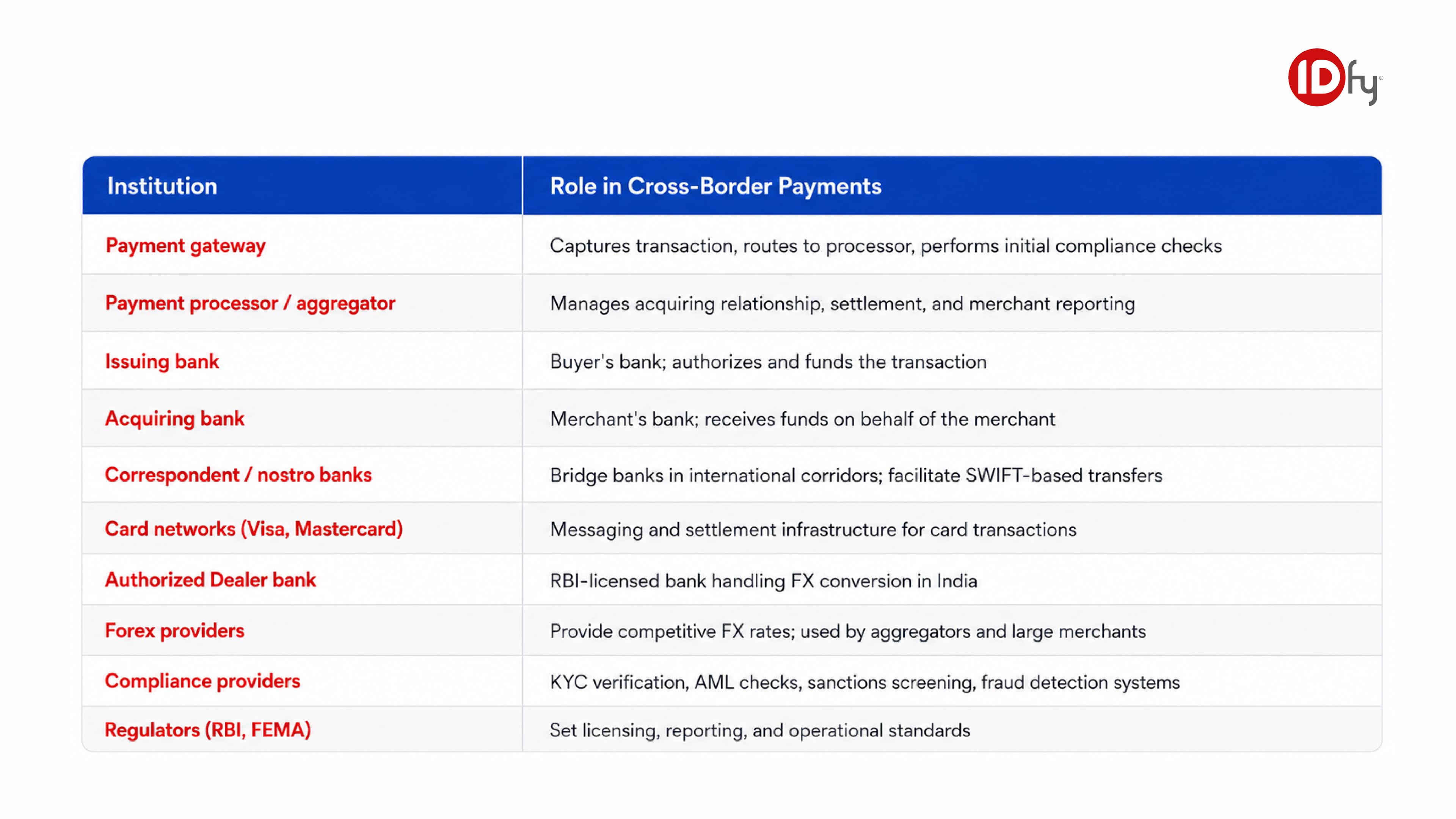

Key Players in the Cross-Border Payment Ecosystem

A single international transaction touches multiple institutions. Each plays a distinct role, and coordination failures between them create the delays and compliance gaps that businesses experience operationally.

Cross-Border Payments Ecosystem: Key Institutions and Their Roles

The involvement of multiple intermediaries is not redundant. Each institution adds a specific function. But each adds a cost layer, a potential delay point, and a compliance checkpoint. Optimizing the payment stack means reducing unnecessary intermediary hops while maintaining regulatory compliance at each stage.

Cross-Border Payment Methods

- SWIFT Transfers

SWIFT (Society for Worldwide Interbank Financial Telecommunication) is the dominant messaging network for high-value bank-to-bank international transfers. It is the standard for B2B invoice payments, large remittances, and trade finance. SWIFT transfers can take 2-5 business days to settle due to correspondent banking chains, and fees can accumulate at each intermediary hop.

For enterprise use cases — large invoice amounts, infrequent transactions, trade credit requirements — SWIFT remains the default. For high-frequency, lower-value transactions, its cost and speed profile makes it less competitive.

- Card Payments (Visa / Mastercard)

International card acquiring allows Indian merchants to accept payments from global buyers holding Visa, Mastercard, American Express, or equivalent cards. This is the primary method for consumer-facing ecommerce, SaaS subscriptions, and digital content platforms.

Cross-border card acquiring introduces specific risks: FX fees applied by issuing banks, chargeback exposure from international buyers, and higher rates of card-not-present fraud. Fraud detection systems calibrated for international transaction patterns are essential for merchants operating in this space.

- Digital Wallets

Wallets like PayPal, Stripe, and regional alternatives provide fast, low-friction international payments — particularly for freelancers and small merchants. Consumer convenience is high. However, wallet-to-bank settlement involves its own compliance and remittance reporting requirements in India.

- Payment Aggregators

Modern payment aggregators — licensed under the RBI's PA-CB (Payment Aggregator - Cross Border) framework — provide API-based payment orchestration that consolidates multiple payment methods, currencies, and settlement workflows into a single integration. For Indian businesses processing international payments at scale, aggregators reduce integration complexity, standardize compliance workflows, and offer settlement optimization across corridors.

Cross-Border Payment Methods Comparison Based on Settlement Speed, Cost, and Compliance Requirements

Regulations Governing Cross-Border Payments in India

India's cross-border payment regulatory architecture rests on two primary frameworks: the Foreign Exchange Management Act (FEMA) administered by the RBI, and the RBI's licensing and reporting requirements for payment intermediaries.

FEMA Guidelines India

FEMA governs all foreign exchange transactions in India. It distinguishes between current account transactions (trade in goods and services, remittances) and capital account transactions (investments, loans). Most business-related cross-border payments — exporter receipts, SaaS subscription collections, freelancer remittances — fall under current account and are subject to defined documentation and reporting norms.

PA-CB Licensing

In 2023, the RBI introduced the Payment Aggregator - Cross Border (PA-CB) licensing framework. Payment aggregators handling cross-border transactions are required to obtain specific authorization. This framework mandates KYC verification of merchants, transaction monitoring, fraud prevention measures, and periodic reporting to the RBI. It effectively formalizes the compliance obligations that were previously inconsistently enforced.

PA-CB licensing has significant implications for fintechs and aggregators: only licensed entities can legally offer cross-border payment aggregation services to Indian merchants. This creates a clear compliance boundary for businesses evaluating their payment provider's regulatory standing.

Documentation Requirements

International payment compliance in India involves specific documentation obligations:

- Form 15CA: A declaration filed by the remitter before making outward remittances above specified thresholds.

- Form 15CB: A certificate from a chartered accountant confirming the applicable tax treatment on the remittance — required for certain payment categories.

- Inward remittance reporting: AD banks are required to report all inward foreign currency receipts. Businesses receiving export proceeds must submit Foreign Inward Remittance Certificates (FIRCs) or equivalent bank-generated documents.

- Purpose codes: Each international transaction must be classified under RBI-defined purpose codes (e.g., P0101 for software exports), which determine regulatory treatment and reporting requirements.

RBI Cross-Border Payment Rules: Key Obligations

- Merchants receiving cross-border payments must be onboarded by a licensed payment aggregator or bank.

- Payment aggregators must conduct KYC verification and KYB verification of merchant businesses before enabling international payment acceptance.

- Export proceeds must be repatriated to India within the timelines prescribed under FEMA (generally within 9 months for goods, which varies by export type).

- All foreign currency receipts must be converted to INR through authorized dealer banks unless specific RBI approval exists for holding foreign currency accounts.

The PA-CB framework is not just a licensing checkbox. It signals the RBI's intent to bring international payment flows under the same compliance rigor as domestic payment systems. For Indian fintechs, regulatory readiness is now a market access condition, not an optional investment.

Operational Challenges in Cross-Border Payments

Despite significant infrastructure improvements, Indian businesses face consistent operational challenges when processing international payments.

Delays from correspondent banking chains

SWIFT-based transfers passing through multiple correspondent banks accumulate delays and fees at each node. For time-sensitive supplier payments or client collections, T+3 to T+5 settlement timelines create working capital tension.

FX volatility

Exchange rate movements between transaction initiation and settlement can erode effective revenue. For businesses invoicing in USD but operating with INR cost structures, unhedged FX exposure is a P&L risk.

Compliance complexity and documentation burden

Maintaining Form 15CA/15CB submissions, purpose code accuracy, and FIRC reconciliation at scale requires dedicated operational resources. Errors in documentation trigger delays, bank queries, or, in serious cases, regulatory scrutiny.

Regulatory fragmentation

Different buyer geographies introduce different local regulatory requirements — GDPR in Europe, FinCEN reporting in the US, MAS guidelines in Singapore. Cross-border commerce teams must navigate this patchwork alongside Indian domestic requirements.

Reconciliation challenges

Matching inbound settlements (which arrive net of fees, FX conversions, and intermediary deductions) to individual transaction records is a significant operational burden for high-volume businesses. Gaps in reconciliation create accounting inaccuracies and tax compliance risk.

Chargebacks and fraud

International card transactions carry higher chargeback rates than domestic transactions. Friendly fraud (illegitimate chargeback claims from buyers) and card-not-present fraud require active fraud detection system investment to manage effectively.

The Role of Compliance and Verification in Cross-Border Payments

As cross-border payment volumes scale, compliance and verification infrastructure becomes the load-bearing layer of the entire stack. This is not a regulatory formality — it is operational risk management.

KYC and KYB Verification

Payment aggregators licensed under the PA-CB framework are required to verify both individual and business customers before enabling international payment acceptance. KYC verification for individuals covers identity document validation, liveness checks, and PAN/Aadhaar linkage. KYB verification for businesses extends to company registration documents, beneficial ownership identification, director verification, and business activity confirmation.

Ongoing due diligence — re-verification at defined intervals and event-triggered reviews — is required for high-risk merchant categories or when transaction patterns change materially.

Weak merchant verification creates systemic risk: it opens the payment network to misuse for money laundering, invoice fraud, or sanctions evasion. Regulators globally, including the RBI, view KYC and KYB verification failures as among the most serious compliance deficiencies.

Fraud Detection Systems

Cross-border transactions have a larger fraud surface than domestic payments. Card-not-present fraud, account takeovers, synthetic identity fraud, and cross-border money mule networks are all active threat categories.

Effective fraud prevention in international payments combines multiple signals:

- Device intelligence: Fingerprinting devices to detect anomalies between declared and actual device characteristics.

- Behavioral analytics: Identifying deviations from established transaction patterns — unusual geographies, atypical payment amounts, new payment methods.

- Velocity monitoring: Detecting unusually high transaction frequency from a single account or payment instrument within defined windows.

- Sanctions screening: Real-time checks against OFAC, UN Security Council, EU, and RBI sanction lists before processing any transaction.

- IP and geolocation analysis: Flagging transactions where the IP address geography does not match the declared buyer location.

International transaction monitoring systems must be tuned for cross-border payment patterns specifically. Domestic fraud models applied without calibration to international transactions generate high false-positive rates, creating unnecessary payment friction for legitimate buyers.

AML Checks

Anti-money laundering obligations for cross-border payment processors are substantial. Under FEMA and the Prevention of Money Laundering Act (PMLA), payment intermediaries must maintain transaction monitoring systems capable of detecting suspicious patterns, file Suspicious Transaction Reports (STRs) with the Financial Intelligence Unit (FIU-IND), and maintain transaction records for prescribed periods.

AML compliance in cross-border payments requires risk-scoring frameworks that factor in transaction size, buyer and seller geography, business category, and transaction frequency. High-risk corridors — countries identified by FATF as having strategic AML deficiencies — require enhanced due diligence.

Conclusion

Cross-border payments are rapidly becoming one of the most operationally consequential capabilities for Indian businesses. The growth of digital exports, global SaaS revenue, and cross-border commerce has moved international payment infrastructure from a niche concern to a core business function.

The regulatory environment in India has evolved to match this growth. PA-CB licensing, FEMA-aligned reporting requirements, and RBI oversight of international payment flows mean that compliance is now inseparable from payment operations. Businesses that treat verification, transaction monitoring, and AML checks as afterthoughts face both regulatory exposure and operational fragility at scale.

The infrastructure challenge is genuinely complex: managing FX exposure, maintaining reconciliation accuracy, meeting documentation requirements, and preventing fraud across multiple geographies simultaneously. But the businesses and fintechs that invest in integrated compliance and payment infrastructure are those that can scale globally with confidence.

As global payment ecosystems evolve, scalable cross-border commerce increasingly depends on integrated identity verification, compliance orchestration, fraud monitoring, and payment infrastructure.

Frequently Asked Questions

What are cross-border payments?

Cross-border payments are transactions where the payer and the recipient are in different countries. They involve currency conversion, multiple banking intermediaries, and compliance requirements across jurisdictions. Examples include Indian SaaS companies collecting USD from overseas clients, freelancers receiving international project payments, and exporters receiving foreign currency against goods or services invoices.

How do cross-border payments work in India?

An international payment initiated by an overseas buyer is routed through a payment gateway or card network to the acquiring bank in India. The acquiring bank or authorized dealer bank converts the foreign currency to INR at the prevailing exchange rate. The INR proceeds are settled into the merchant's account, typically within T+1 to T+5 depending on the payment method. The entire process must comply with FEMA guidelines and RBI reporting requirements.

What RBI rules apply to international payments?

Indian businesses receiving international payments must work with RBI-authorized payment aggregators or banks. Export proceeds must be repatriated within prescribed FEMA timelines. All foreign currency receipts must be classified under defined purpose codes. Outward remittances above threshold amounts require Form 15CA and, where applicable, Form 15CB filings. Payment aggregators handling cross-border transactions must hold PA-CB authorization from the RBI.

What is PA-CB licensing?

PA-CB (Payment Aggregator - Cross Border) is an RBI licensing framework introduced in 2023 for entities facilitating cross-border payment aggregation. Licensed PA-CBs can enable Indian merchants to accept international payments. The licensing requires applicants to demonstrate KYC/KYB verification capabilities, fraud detection systems, transaction monitoring, and minimum net worth. Only PA-CB licensed entities can legally provide cross-border payment aggregation services in India.

Why is KYC verification important in cross-border payments?

KYC verification establishes the identity of individuals and businesses initiating or receiving international payments. In cross-border contexts, it prevents the payment network from being misused for money laundering, trade-based fraud, and sanctions evasion. Regulatory frameworks including FEMA, PMLA, and the PA-CB licensing norms mandate KYC verification as a prerequisite for merchant onboarding. KYB verification adds a business-specific layer: verifying company registration, beneficial ownership, and the legitimacy of the declared business activity.

How do businesses prevent fraud in international payments?

Effective fraud prevention combines multiple layers: real-time sanctions screening, device and behavioral intelligence to detect anomalies, velocity monitoring to identify unusual transaction patterns, and geolocation checks. For card-based international payments, 3D Secure authentication adds an additional verification layer. Payment providers managing cross-border transactions at scale use machine learning-based fraud detection systems trained on international transaction data, with risk thresholds calibrated separately from domestic payment models.

Explore how IDfy’s integrated KYC verification, KYB verification, and transaction monitoring infrastructure can support your cross-border payment operations and compliance requirements.

Learn important payment terms in simple language. Understand UPI, BNPL, Payment Gateways, Merchant Onboarding, and more with our easy 2026 guide.

Explore the 2026 payment fraud landscape in India. Learn the most common types of payment fraud, the emerging fraud trends, and how to build a future-ready fraud prevention strategy.

Learn how BNPL works in India, its risks, regulations, business models, and future trends in digital payments and embedded finance.